change means opportunity I

my goal with this (now 125+ page!) schpeel was to say that the economic covenant of the internet is breaking. we’re witnessing the end of a 30-year handshake deal that built the modern web. there’s a $316B search advertising bubble that’s about to pop. When AI agents browse the web on our behalf, never clicking through to websites, the entire economic model that funds the internet no longer works.

But change means opportunity. The collapse of the old model creates space for new ones. AI-native commerce, agentic interfaces, memory-driven personalization, and collaborative human-AI workflows represent enormous opportunities for those who build the infrastructure of what comes next. The window is narrow. The platforms that will define the next era of the internet are being built right now, by teams that understand both the depth of what’s breaking and the audacity required to build its replacement.

22,100. Thats the amount of musicians that made over $50k in royalties from spotify in 2024. thats a livable wage, and certainly couldnt have been possible ‘in the old days’. its def gotten better. the 100,000th-ranked artist on Spotify has seen their generated royalties multiply by over 10x (increasing from well under 600 USD in 2014 to almost 6,000 USD in 2024). but there are sooo many more artists (12 million) who are pursuing their creative passions (in reality its much more that aren’t on the platform), and earn almost nothing, trapped in a system where platforms extract the lion’s share of value while dangling the promise of discovery and audience reach.

most would point their finger at the platform and labels to yap that they squeeze all the revenue for themselves. this is why taylor swift wanted to separate from her label and pursue her independence, and why kanye, jayz, madonna etc created their own streaming company. It’s the same reason nebula was spun up by youtube creators: they were tired of losing nearly half of their potential revenue. patreon - headed by my fav cover band pomplamoose/scary pockets leader jack conte – was a last ditch resort to find new ways to compensate creators (akin to donationware in oss). These platforms represent early attempts to escape the coming collapse, but theyre rearranging deck chairs on the titanic.

it feels like everything is about to break. implode. a massive bubble is imminent. im not sure we realize what it means for the future of the social and economic contracts that have been at the base of how the internet works since its inception. hundreds of billions are at stake.

The first internet banner ad was bought by AT&T in 1994. This ad appeared on the website HotWired, which was the online version of Wired magazine. It marked the beginning of online advertising, a pivotal moment that has since evolved into a massive industry (~73% of $1.1T, 9% CAGR, most of which is going towards ‘the big five’, aka Big Tech). In 2017 it was already “massive” at $83B and 16% growth rate.

This digital advertising model, which powers ‘the big five’, is about to fking explode.

the incentive structure of internet has been driven by the handshake promise that google can use my content in return for traffic to my website where i can thereafter sell goods / services. we would add a robots.txt and cookies.txt that allow part of my website to be scraped and users to be tracked so that google could list me on their discovery engine, since navigating every website would be too cumbersome for a user. you can of course replace google with any of the other big five: meta, amazon, microsoft, and alibaba.

the idea is that once a google user is on my website, i could upsell them for other goods/services, like bundling nike shoes and socks for ‘marathon personas’, or insurance premiums for your home, roof and pet frog. this is the unwritten rule of loss leaders, hero products and accenture’s methodology of getting a foot in the door.

Brands pay exorbitant amounts to rank at the top for keywords like shampoo, Chinese food, and accounting firms so that they have the opportunity to fulfill the product/service request (and upsell) thereafter. Companies that didn’t join this race often got overshadowed by those that did, as seen with the success of Zappos in online shoe retail, NYT with SEO headlines, and TripAdvisor in tourism. Much more on this later

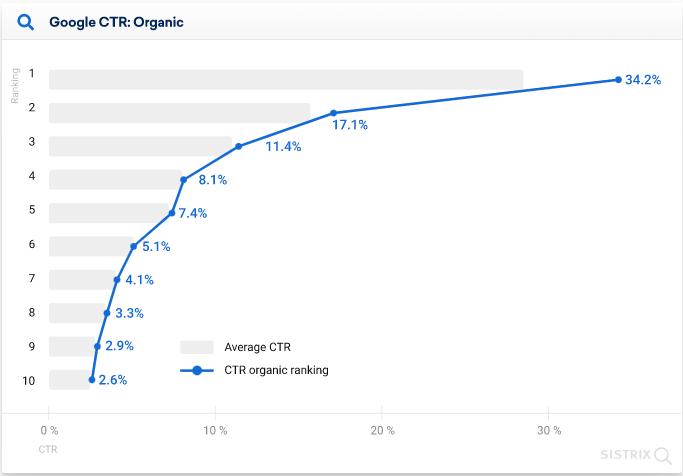

Figure: 96.2% of all clicks are on one of the top 10 links.

concretelely, a human inputs a few words and the genie search platform will conjure 10 blue links for users to navigate until they find their answer. for decades this was called ‘googling’. If you multiply the estimated 13 to 16 billion daily searches google processes daily by the 17.1% boost of being the top ranked link, it makes sense that brands pay in aggregate ~$175 billion in search ad revenue to drive traffic to their site.

But if a Google AI Overview or ChatGPT agent browses on the user’s behalf and returns the answer, why would the human continue onto the brand websites? this is the dramatic threat. Sama says they’re now handling a staggering 2.5 billion prompts every day, with 330 million daily queries coming from the U.S. alone. This is 1/6th of google’s volume. 8 months ago that figure was <1B … what rate will this continue to grow at?

in the future there is no reason for the customer to continue onto the website once theyve retrieved their answer. this is the catalyst for the implosion.

we are getting the answer and then moving on.

is this inevitable? what is required to enable this? what does it mean for the future of commerce, advertising and user experiences? Is there a generational startup opportunity? I’m not sure, but I’d like to find out.

history

In the beginning there was nothing. big primordial void. im gonna skip ahead a couple years past the grunting apes to when we codified a set of sounds to represent observed objects and experiences. Functionally, we were communicating (transferring) information: nearby danger, territorial claims, etc. This happened mostly orally, with some hand waving and a lot of bonking.

To no ones modern surprise, the scalability of conveying information to the entire population orally is infeasible within a life time. some bloke was fed up with managing record keeping through a game of telephone and decided to write onto a slab of rock the Kish tablet. Writing is important because it unlocked the rate at which information could be consumed. 2(+) people could read it at the same time. at any point in the day. without blud even being there. plus the information was (literally) set in stone - no one could mishear things.

However, writing itself had a bottleneck: duplication. To reach a wider audience, written material had to be manually copied or moved, which limited the dissemination of ideas. for a couple thousand years, ppl would just show up to the town square or have many scribes reproduce the works - no wonder so many religious monks had commentaries on the commentaries. The invention of the printing press unlocked duplication by stamping the same pages over and over. This is particularly important because (until 1440 - tho china figured it out in the 800s) only powerful institutions with the manpower could disseminate (and contril) ideas. to no ones postmodern surprise, the second major use of the printing press was porn.

Ok now we got consumable information, duplicatable at close to 0 marginal cost. the next bottleneck was

distribution: getting written information into the hands of the public was still a complex task. steam-powered printing presses drastically reduced the cost of printing and enabled newspapers to produce large volumes of copies at a lower price. The “Relation aller Fürnemmen und gedenckwürdigen Historien” in Germany, and the “Gazette” in France, provided regular updates on news, events and information to the masses.

The bottleneck of distribution gradually got less restrictive until the internet made distribution virtually free and accessible to everyone. Additionally, it was global. There were no physical or geographical limitations anymore. This is a major crux of this manifesto: infinite distribution + commoditization = personalization.

Before we go any further, there is an important milestone that I jumped over. Between the written mediums of newspapers and the internet, there existed (still exists?) the proliferation of ideas and information through radio and television. This is very very noteworthy because (for the first time outside of church) we would hear (and eventually see) information directly from its source, immediately. no next day paper. now.

There still remains two challenge: the creation and substantiation of ideas. while I can have numerous ideas and the Internet allows me to distribute them globally, I still need to write them down, just as artists need to create images and musicians need to compose songs. It is becoming increasingly evident that this bottleneck is also on the brink of being eliminated. Ill get to this later, but tldr: AI.

the history of ads

One of the earliest known ads was found in Thebes, Egypt, promoting a reward to capture and return a runaway slave named Shem. Since then, we have paid a very heavy price.

During the 1500s, print ads mainly focused on promoting events, plays, concerts, and products like books and medicines.

The first newspaper advertisement was published on April 17, 1704, in the Boston News-Letter, promoting an estate for sale. In 1741,

none other than the face of the $100 bill himself, pioneered magazine advertising in his ‘General Magazine’ booklet. Ben, frankly, this was a founding moment. In 1835, the very first billboard advertisement was created by Jared Bell in New York to promote Barnum & Bailey Circus.tbt to when zoos were cool and exotic

In 1841, Volney B. Palmer, the first ad agency, was established in Philadelphia. Instead of having to sell ads and build relationships with multiple newspapers, advertisers could work with the ad agency, which could leverage its connections with all those newspapers and serve multiple clients.

Radio gained significant popularity during and after World War II, but the first paid radio ad aired on August 22, 1922, on the New York City radio station, WEAF. The 15-minute ad, paid for by a real estate company called the Queensboro Corporation, promoted apartments in Jackson Heights, Queens. Later, the first television commercial aired in 1941 by the Bulova Watch Company. You can watch it here. It was ten seconds long and viewed by ~4,000 people in New York (#viral?).

The usefulness of ad agencies only grew as more advertising formats like radio and TV emerged. Particularly with TV, advertisers not only needed to place ads but also required significant help in creating them; ad agencies invested in ad-making expertise because they could apply this expertise across multiple clients. This led to the Golden Age of Advertising, where businesses made substantial investments in advertising to convey their brand’s uniqueness and engage their target audience.

Simultaneously, advertisers were rapidly expanding their geographic reach, especially after the Second World War; naturally, ad agencies expanded their reach as well, often through mergers and acquisitions. The primary business opportunity remained the same: provide advertisers with a one-stop shop for all their advertising needs.

Years later, after the development of ARPANET (1960s) and the World Wide Web (1989), the first online display ad was created in 1994 by AT&T, which asked users, “Have you ever clicked your mouse right HERE?” with an arrow pointing to text that read “YOU WILL.” The ad achieved a click-through rate of 44% - a figure that would astonish modern-day marketers. Fitting that the first ad was clickbait.

but why do ads actually work???

When the Internet came along, with its infinite distribution to infinite users, the newspapers, brands, and ad agencies were pumped af: more users = more money! Ad agencies in particular were frothing as more channels means more complexity and the ad agencies could abstract that away for their clients!

Before the Internet, a newspaper like the New York Times was limited in reach; now it can reach anyone on the planet! The problem for publishers, though, is that the free distribution provided by the Internet is not an exclusive. It’s available to every other newspaper as well. Moreover, it’s also available to publishers of any type. In the early internet (and to this day) individuals could post their own news updates, and to the indifferent HTML protocol, it was on ‘completely equal footing’.

That abundance of publications (blogs, webpages, brandsites, etc) meant that discovery was far more important than distribution.

So, two kids in a garage in palo alto decide to invent a way to rank pages, aptly called PageRank. Actually, much like the printing press, the groundwork was done in china. The first successful strategy for site-scoring and page-ranking was link analysis: ranking the popularity of a web site based on how many other sites had linked to it. Robert Li’s RankDex was created in 1996, filed for patent in 1997, granted in 1999, and then he used it to found Baidu in 2000. Larry Page referenced Robin Li’s work in the citations for PageRank.

Increasingly users congregated on two discovery platforms: Google for things for which they were actively looking, and Facebook for entertainment.

IRL

Start with the top 25 advertisers in the U.S. The list is made up of:

4 telecom companies (AT&T, Comcast, Verizon, Softbank/Sprint)

4 automobile companies (General Motors, Ford, Fiat Chrysler, Toyota)

4 credit card companies (America Express, JPMorgan Chase, Bank of America, Capital One)

3 consumer packaged goods (CPG) companies (Procter & Gamble, L’Oréal, Johnson & Johnson)

3 entertainment companies (Disney, Time Warner, 21st Century Fox)

3 retailers (Walmart, Target, Macy’s)

1 from electronics (Samsung), pharmaceuticals (Pfizer), and beer (Anheuser-Busch InBev)

Before going into Google and Facebook’s operating models more deeply, lets look to a more simple analog example. Buying the swiffer (Procter & Gamble’s cleaning mop stick thingy) in a Target. why do we decide to do so?

Ad agencies would say it is due to successful guidance through the Purchase Funnel, a concept initially introduced in 1925 in Edward Strong’s book, The Psychology of Selling and Advertising. The funnel is composed of: “attention, interest, desire, action, satisfaction”.

The real credit goes to E. St. Elmo Lewis, who in 1898 introduced the slogan, “Attract attention, maintain interest, create desire,” during an advertising course he taught in Philadelphia. He mentioned that he derived the idea from studying the psychology of William James. Later, he expanded the formula to include “get action.” Around 1907, A.F. Sheldon further enhanced it by adding “permanent satisfaction” as a crucial element. Although few in 1907 recognized the importance of this last phrase, today it is widely acknowledged as essential for providing service, gaining the buyer’s goodwill, meeting their needs, and ensuring lasting satisfaction.

Anyway,

- Attention: make the buyer aware of a problem they have

- Interest: the buyer becomes interested in solving their problem

- Desire: the buyer becomes interested in your solution to their problem

- Action: the buyer acquires your solution

A classic example of the complete AIDA model condensed into a single commercial is this roll-out campaign for the Swiffer mop

The entire funnel is encapsulated in this ad:

- Attention: Traditional cleaning methods stir up dirt

- Interest: Dirt needs to be removed, not just moved

- Desire: Swiffer cloths collect dirt and can be thrown away

- Action: Find Swiffer in the household cleaning aisle

The reference to the aisle is crucial: shelf space has long been the cornerstone for large consumer packaged goods companies. Swiffer achieved widespread distribution immediately upon launch because P&G could leverage its other popular products during negotiations with retailers like Walmart and Target to secure the best shelf location placement. Importantly, simply being on shelves increases the likelihood that customers will discover you independently or recognize you after repeated exposure. in ‘traditional retail advertising’ shelf space provided both distribution and discovery.

Notice that the vast majority of the industries on the list are dominated by massive companies that compete on scale and distribution. CPG is the perfect example: building a “house of brands” allows a company like Procter & Gamble to leverage scale to invest in R&D, reduce the cost of products, and target demographic groups without perfect personalization. TV is the perfect medium to cater to the masses. In fact, the top 200 advertisers in the U.S love TV so much that they make up 80% of television advertising, despite accounting for only 51% of total advertising spend (and 41% of digital).

Linear television and its advertisers were fundamentally based on controlling distribution (i.e. retail shelf space) and thereby controlling customers.

Many of the companies on this list are now under threat from the Internet. When supply was limited by physical space, shelves were highly valuable for both discovery and distribution. But with the Internet making shelf space virtually limitless, these brands can no longer monopolize the once-scarce shelf space. and I’m no mathematician, but it’s clear that trying to dominate an infinite space is a losing battle. Specifically:

- CPG companies face threats on two fronts: on the high end, the combination of e-commerce and highly-targeted, highly-measurable Facebook advertising has led to a rise in boutique CPG brands offering superior products to very specific groups. On the low end, e-commerce not only diminishes the shelf-space advantage but also sees Amazon making significant moves into private label products.

- Similarly, big box retailers that offer little beyond availability and low prices are being surpassed by Amazon in both areas. In the long term, it’s difficult to see how they will continue to survive.

- Automobile companies, on the other hand, are dealing with three distinct challenges: electrification, transportation-as-a-service (like Uber), and self-driving cars. The latter two, in particular (and to some extent the first), suggest a future where cars become mere commodities purchased by fleets, making advertising to customers obsolete.

Many of these major companies, consciously, unconsciously, or under the veil of ‘Hate Speech’, decided to boycott Facebook in 2020. Household brands like Coca-Cola, J.M. Smucker Company, Diageo, Mars, HP, CVS Health, Clorox, Microsoft, Procter & Gamble, Samsung, Walmart, Geico, Hershey and 1000 others decided to pull their spending on the app. Seems like a major blow, right? Zuckerberg was unphased.

For reference, 2019 Facebook’s top 100 advertisers made up less than 6% of the company’s ad revenue. Most of the $69.7 billion the company brought in came from its long tail of 8 million advertisers. This explains why the news about large CPG companies boycotting Facebook is, from a financial perspective, simply not a big deal.

Unilever’s measly $11.8 million in U.S. ad spend, to take one example, is replaced with the same automated efficiency that Facebook’s timeline ensures you never run out of content. Facebook loses some top-line revenue – in an auction-based system, less demand corresponds to lower prices. And yet, due to these lower prices, smaller direct-to-consumer companies can now bid and steal customers from massive conglomerates like Unilever. The content will be filled regardless, and the markets are very efficient.

The unavoidable truth is that TV advertisers are 20th-century entities: designed for mass markets, not niches, designed for brick-and-mortar retailers, not e-commerce. These companies were built on TV, and TV was built on their advertisements. While they are currently supporting each other, the decline of one will accelerate the decline of the other. For now, the interdependence of these models is keeping them afloat, but it only means that when the end comes, it will arrive more quickly and broadly than anyone anticipates.

Online

the traditional marketing funnel made sense in a world where different parts of the customer journey happened in different places — literally. You might see an advertisement on TV, then a coupon in the newspaper, and finally the product on an end cap in a store. Every one of those exposures was a discrete advertising event that culminated in the customer picking up the product in question in putting it in their (literal) shopping cart.

One of the hallmarks of the Internet is that the entire AIDA funnel can be often compressed into a single Facebook ad that you might only see for a fraction of a second; perhaps something will catch your eye, and you will swipe to see more, and if you are intrigued, you can complete the purchase right then and there. The journey is increasingly compressed into a single impression: you see an ad on Instagram, you click on it to find out more, you login with Shop Pay, and then you wonder what you were thinking when it shows up at your door a few days later. The loop for apps is even tighter: you see an ad, click an ‘Install’ button, and are playing a level just seconds later. Sure, there are things like re-targeting or list building, but by-and-large Internet advertising, particularly when it comes to Facebook, is almost all direct response. You might even forget about your purchase right up until a mysterious package shows up at your door a few days later.

Due to the format of these ads, digital advertising has worked much better for direct response marketing. Aka impulse purchases. Notice how this is a very different commerce behavior than having gone to Target, motivated by a TV ad + newspaper coupon, to examine the physical usefulness. Now:

- Facebook helps find the customers

- Shopify or WooCommerce build the storefronts

- Stripe or PayPal handle payments

- Third-party logistics providers package and ship the goods

- USPS, Fedex, and UPS deliver the actual packages

In the same way that the internet made the distribution and duplication of content indiscriminantly, facebook ads allows anyone to put an ad that can reach anyone. This has the same effect of creating perfect competition.

Here is the problem for DTC commerce: Facebook really is better at finding brands’ customers than anyone else. This alludes to Zuck’s endgame, but essentialy DTC ad budgets are forced onto facebook as it is the best (measured) return-on-investment for acquired customers on Facebook, where DTC companies are competing against all of the other DTC companies and mobile game developers and incumbent CPG companies and everyone else for user attention. That means the real winner is Facebook, while DTC companies are slowly choked by ever-increasing customer acquisition costs. Facebook is the company that makes the space work, and so it is only natural that Facebook is harvesting most of the profitability from the DTC value chain.

What made the Facebook model work is that the Meta Pixel (now CAPIs) could map a conversion (downloading of an app/purchasing the swiffer) to ad-targeted customers on their social media app. because Facebook knew a lot about someone who saw each ad and thereafter converted, they created an algorithm in 2013 that could easily find other people who were similar and show them similar ads (lookalike audiences). Along with the news feed, this was one of the biggest moments in Facebook’s history. From then on, they could use the data flywheel to continually optimizing their targeting and increasing their understanding along the way. Now Advantage+ is essentially a 1-click “set it and forget it”.

This has fundamentally changed the plane of competition: no longer do distributors compete based upon exclusive supplier relationships, with consumers/users an afterthought. Instead, suppliers can be commoditized leaving consumers/users as a first order priority. By extension, this means that the most important factor determining success is the user experience: the best distributors/aggregators/market-makers win by providing the best experience, which earns them the most consumers/users, which attracts the most suppliers, which enhances the user experience in a virtuous cycle.

Ben Thompson, Aggregation Theory (2015)

To be fair to the DTC companies, they are hardly the first to make this mistake: when the internet newspapers looked at the Internet and only saw the potential of reaching new customers; they didn’t consider that because every other publisher in the world could now reach those exact same customers, the integration that drove their business — publishing and distribution in a unique geographic area — had disintegrated. For a (long) time, Newspapers dominated both editorial and advertisements, but it turns out that was simply a function of who owned printing presses and delivery trucks; once the Internet came along advertisers, which cared about reaching customers, not supporting journalists, switched to Facebook and Google, which had aggregated the former and commoditized the latter. It is the same lesson that TV-era brands are facing now that they can’t just win by dominating shelf space. If some part of the value chain becomes free, that is not simply an opportunity but also a warning that the entire value chain is going to be transformed. How will brands adapt?

https://stratechery.com/2020/email-addresses-and-razor-blades/

Facebook, Amazon, Netflix, and Google (plus Uber/Airbnb etc) are structurally very similar companies: all leveraged zero distribution costs and zero transaction costs to own users at scale via a superior experience that commoditized suppliers and let them skim off the middle, either through fees, subscriptions, and/or ads.

Google, though, has a built-in advantage: Google doesn’t have to figure out what you are interested in because you do the company the favor of telling it by searching for it. The odds that you want a hotel in San Francisco are rather high if you search for “San Francisco hotels”; it’s the same thing with life insurance or car mechanics or e-commerce.

Amazon goes a step further and has effectively integrated the entire e-commerce stack when it comes to the distribution of goods consumers are explicitly searching for:

- Customers come to Amazon directly

- Searches on Amazon lead to Amazon product pages or 3rd-party merchant listings that look identical to Amazon product pages

- Amazon handles payments

- Amazon packages and ships the goods

- Amazon increasingly delivers the actual packages

This is great for aggregators like Google and Amazon, but not so great for P&G: remember, dominating shelf space was a core part of their strategy, and Amazon and Google have infinite shelf space! Anyone can publish, and this creates perfect competition - terrible for suppliers who face commoditization and shrinking margins, but great for consumers who enjoy more choices and lower prices.

gaming the algorithms

There are two big challenges when it comes to winning search:

- You need to rank for the right keywords - This means understanding what your customers are actually searching for, not what you think they should be searching for

- You need to rank for the right keywords at the right time - This means understanding when your customers are most likely to be searching for your product or service

The first challenge is about keyword research and understanding your customer’s search behavior. The second challenge is about timing and understanding when your customers are most likely to be in a buying mood.

For example, if you’re selling winter coats, you want to rank for “winter coats” in the fall and winter, not in the spring and summer. If you’re selling tax software, you want to rank for “tax software” in January through April, not in the summer.

The key is to understand your customer’s buying cycle and align your SEO strategy with it. This means:

- Researching when your customers are most likely to search for your product

- Creating content that addresses their needs at different stages of the buying cycle

- Optimizing your website for the keywords they’re most likely to use

- Building backlinks from relevant websites in your industry

The goal is to be there when your customers are ready to buy, not when you’re ready to sell.

- Because search is initiated by the customer, you want that customer to not just recognize your brand (which is all that is necessary in a physical store), but to also recall your brand (and enter it in the search box). This is a much stiffer challenge and makes the amount of time and money you need to spend on a brand that much greater.

- If prospective customers do not search for your brand name but instead search for a generic term like “laundry detergent” then you need to be at the top of the search results. And, the best way to be at the top is to be the best-seller. In other words, having lots of products in the same space can work against you because you are diluting your own sales and thus hurting your search results.

In order to survive on the Internet, an ugly truth was emerging. One has to cater to Google. They have all the customers. Yelp and countless other sites depend on Google to bring them web traffic — eyeballs for their advertisers.

This creates a dependency problem: if Google changes its algorithm, your traffic can disappear overnight. This is exactly what happened to many websites when Google updated its algorithm to favor mobile-friendly sites, or when it started prioritizing user experience metrics like page speed and Core Web Vitals.

The solution is to diversify your traffic sources and not rely solely on Google. This means:

- Building an email list

- Creating content for social media platforms

- Developing partnerships with other websites

- Investing in paid advertising on multiple platforms

- Creating a strong brand that people remember and search for directly

The key is to build a sustainable business that doesn’t depend on any single platform or algorithm change.

Yelp, like many other review sites, has deep roots in SEO — search-engine optimization. Their entire business was long predicated on Google doing their customer acquisition for them. This meant a heavy emphasis on both speed and SEO, and an investment in anticipating and creating content to answer consumer questions. This includes using tools like SemRush and hiring SEO-specialized ad agencies to flourish online. And to their credit, since their founding in 2004, they’ve had great success in being the destination website for restaurant reviews and the sort.

You may think, are does anything even change if you play the SEO game? The answer is a big-time yes. Even a small boost at the scale at which google operates (13.7B searches/day, 5T/year), would be huge.

But here’s the thing: SEO is a zero-sum game. For every website that moves up in the rankings, another one moves down. This creates a constant arms race where everyone is trying to out-optimize everyone else, but the total amount of traffic available stays roughly the same.

This is why we’re seeing the shift to AI-powered search results. Google is trying to break out of this zero-sum game by providing direct answers instead of just links. But this creates new problems, as we’ll explore in the next sections.

The fundamental issue is that the internet has made distribution free, but it hasn’t made attention free. There’s still only so much attention to go around, and everyone is competing for it. The question is: how do we create a more sustainable system that doesn’t require constant optimization and gaming?

| Google Search Feature | Click Through Rate (CTR) |

|---|---|

| Ad Position 1 | 2.1% |

| Ad Position 2 | 1.4% |

| Ad Position 3 | 1.3% |

| Ad Position 4 | 1.1% |

| Search Position 1 | 39.8 § |

| Search Position 2 | 18.7% §§ |

| Search Position 3 | 10.2% |

| Search Position 4 | 7.2% |

| Search Position 5 | 5.1% |

| Search Position 6 | 4.4% |

| Search Position 7 | 3.0% |

| Search Position 8 | 2.1% |

| Search Position 9 | 1.9% |

| Search Position 10 | 1.6% |

- § If snippet, then 42.9%; If AI overview, then 38.9%; If local pack present, then 23.7%

- §§ If snippet, then 27.4%; If AI overview, then 29.5%; If local pack present, then 15.1%

Source: First Page Sage

But the data is more than just a small boost - the jump from 18.7% to 27.4% CTR is massive. For most companies, going from search position 8 to search position 3 (or vice versa) can make or break a business.

But AI Overviews (AIO) are existential threats to companies like Yelp. Look at what Chegg wrote in their 2024 Annual Financial Report:

While we made significant headway on our technology, product, and marketing programs, 2024 came with a series of challenges, including the rapid evolution of the content landscape, particularly the rise of Google AIO, which as I previously mentioned, has had a profound impact on Chegg’s traffic, revenue, and workforce. As already mentioned, we are filing a complaint against Google LLC and Alphabet Inc. in the U.S. District Court for the District of Columbia, making three main arguments. We allege in our complaint, Google AIO has transformed Google from a “search engine” into an “answer engine,” displaying AI-generated content sourced from third-party sites like Chegg. Google’s expansion of AIO forces traffic to remain on Google, eliminating the need to go to third-party content source sites. The impact on Chegg’s business is clear. Our non-subscriber traffic plummeted to negative 49% in January 2025, down significantly from the modest 8% decline we reported in Q2 2024.

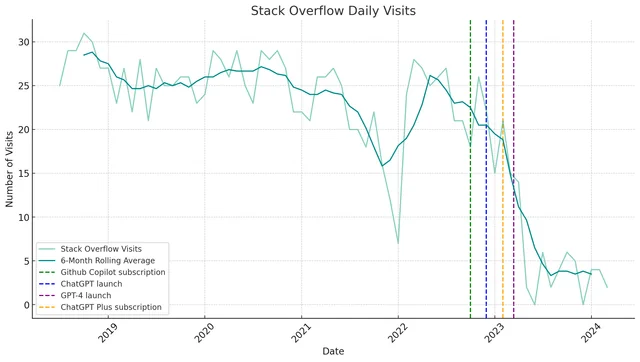

Theyre not the only one, Stack Overflow has taken a massive hit too. These companies relied on the handshake promise that google can use my content in return for traffic to my website where i can thereafter sell goods / services. Or at the very least display banner ads on their website.

In a 2014 video that Yelp put out, while it makes many of the same arguments as the Chegg lawsuit, instead of being focused on regulators it is targeting Google itself. They argue that Google isn’t living up to its own standards by not featuring the best results, and not driving traffic back to sites that make the content Google needs (by, for example, not including prominent links to the content filling its answer boxes; Yelp isn’t asking that they go away, just that they drive traffic to 3rd parties). Google may be an aggregator, but it still needs supply, which means it needs a sustainable open web.

Yelp, Chegg and Stack Overflow are not the first and not the last to be at the whims of Google. Back in 2006, Belgian news publishers sued Google over their inclusion in the Google News, demanding that Google remove them. After winning the initial suit, Google dropped them as demanded. Then the publications, watching their traffic drop dramatically, scrambled to get back in. That same year’s Field v. Google held that Google’s usage of snippets of the plaintiff’s content was fair use, and furthermore, that Blake Fields, the author, had implicitly given Google a license to cache his content by not specifying to Google to not crawl his website.

In 2014, A group of German publishers started legal action against the search giant, demanding 11 percent of all revenue stemming from pages that include listings from their sites. In the case of the Belgian publishers in particular, it was difficult to understand what they were trying to accomplish. After all, isn’t the goal more page views (it certainly was in the end!)? The German publishers in this case are being a little more creative: like the Belgians before them they are alleging that Google benefits from their content, but instead of risking their traffic by leaving Google, they’re instead demanding Google give them a cut of the revenue they feel they deserve.

The obvious reaction to this case, as with the Belgian one, is to marvel at the publisher’s nerve; after all, as we saw with the Belgians, Google is the one driving traffic from which the publishers profit. “Ganz im Gegenteil!” say the publishers. “Google would not exist without our content.” And, at a very high level, I suppose that’s true, but it’s true in a way that doesn’t matter, and understanding why it doesn’t matter gets at the core reason why traditional journalistic institutions are having so much trouble in the Internet era.

The ugly truth, though, as these newspaper publishers found out, is that not being in Google means a dramatic drop in traffic. No website can afford to exclude Google’s crawler from robots.txt because it would be economically ruinous. AI Overviews snippets in search (Google’s defense against AI-chatbot incursions into their search dominance) requires that if you want your content available to Google Search — and any publisher must — then your content will go into Google’s most important AI product as well.

Not everyone wants to play into Google’s game, though. Even when their ad business tanked 30% around the same time snippets were introduced, the New York Times wrote:

We are, in the simplest terms, a subscription-first business. Our focus on subscribers sets us apart in crucial ways from many other media organizations. We are not trying to maximize clicks and sell low-margin advertising against them. We are not trying to win a pageviews arms race. We believe that the more sound business strategy for The Times is to provide journalism so strong that several million people around the world are willing to pay for it. Of course, this strategy is also deeply in tune with our longtime values. Our incentives point us toward journalistic excellence … [yet] our journalism must change to match, and anticipate, the habits, needs and desires of our readers, present and future.

That raises the question as to what are the vectors on which “destination sites” — those that attract users directly, independent of the Aggregators — compete? The obvious two candidates are focus and quality. What is important to note, though, is that while quality is relatively binary, the number of ways to be focused — that is, the number of niches in the world — are effectively infinite; success, in other words, is about delivering superior quality in your niche — the former is defined by the latter.

The transformative impact of the Internet is only starting to be felt, which is to say that the long run will be less about traditional companies adopting digital than it will be about their entire way of doing business being rendered obsolete.

Continue: change means opportunity II