change means opportunity

my goal with this (now 125+ page!) schpeel was to say that the economic covenant of the internet is breaking. we’re witnessing the end of a 30-year handshake deal that built the modern web. there’s a $316B search advertising bubble that’s about to pop. When AI agents browse the web on our behalf, never clicking through to websites, the entire economic model that funds the internet no longer works.

But change means opportunity. The collapse of the old model creates space for new ones. AI-native commerce, agentic interfaces, memory-driven personalization, and collaborative human-AI workflows represent enormous opportunities for those who build the infrastructure of what comes next. The window is narrow. The platforms that will define the next era of the internet are being built right now, by teams that understand both the depth of what’s breaking and the audacity required to build its replacement.

22,100. Thats the amount of musicians that made over $50k in royalties from spotify in 2024. thats a livable wage, and certainly couldnt have been possible ‘in the old days’. its def gotten better. the 100,000th-ranked artist on Spotify has seen their generated royalties multiply by over 10x (increasing from well under 600 USD in 2014 to almost 6,000 USD in 2024). but there are sooo many more artists (12 million) who are pursuing their creative passions (in reality its much more that aren’t on the platform), and earn almost nothing, trapped in a system where platforms extract the lion’s share of value while dangling the promise of discovery and audience reach.

most would point their finger at the platform and labels to yap that they squeeze all the revenue for themselves. this is why taylor swift wanted to separate from her label and pursue her independence, and why kanye, jayz, madonna etc created their own streaming company. It’s the same reason nebula was spun up by youtube creators: they were tired of losing nearly half of their potential revenue. patreon - headed by my fav cover band pomplamoose/scary pockets leader jack conte – was a last ditch resort to find new ways to compensate creators (akin to donationware in oss). These platforms represent early attempts to escape the coming collapse, but theyre rearranging deck chairs on the titanic.

it feels like everything is about to break. implode. a massive bubble is imminent. im not sure we realize what it means for the future of the social and economic contracts that have been at the base of how the internet works since its inception. hundreds of billions are at stake.

The first internet banner ad was bought by AT&T in 1994. This ad appeared on the website HotWired, which was the online version of Wired magazine. It marked the beginning of online advertising, a pivotal moment that has since evolved into a massive industry (~73% of $1.1T, 9% CAGR, most of which is going towards ‘the big five’, aka Big Tech). In 2017 it was already “massive” at $83B and 16% growth rate.

This digital advertising model, which powers ‘the big five’, is about to fking explode.

the incentive structure of internet has been driven by the handshake promise that google can use my content in return for traffic to my website where i can thereafter sell goods / services. we would add a robots.txt and cookies.txt that allow part of my website to be scraped and users to be tracked so that google could list me on their discovery engine, since navigating every website would be too cumbersome for a user. you can of course replace google with any of the other big five: meta, amazon, microsoft, and alibaba.

the idea is that once a google user is on my website, i could upsell them for other goods/services, like bundling nike shoes and socks for ‘marathon personas’, or insurance premiums for your home, roof and pet frog. this is the unwritten rule of loss leaders, hero products and accenture’s methodology of getting a foot in the door.

Brands pay exorbitant amounts to rank at the top for keywords like shampoo, Chinese food, and accounting firms so that they have the opportunity to fulfill the product/service request (and upsell) thereafter. Companies that didn’t join this race often got overshadowed by those that did, as seen with the success of Zappos in online shoe retail, NYT with SEO headlines, and TripAdvisor in tourism. Much more on this later

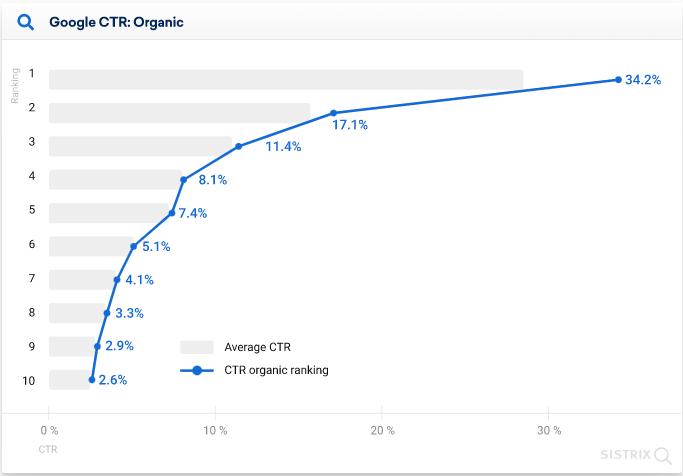

Figure: 96.2% of all clicks are on one of the top 10 links.

concretelely, a human inputs a few words and the genie search platform will conjure 10 blue links for users to navigate until they find their answer. for decades this was called ‘googling’. If you multiply the estimated 13 to 16 billion daily searches google processes daily by the 17.1% boost of being the top ranked link, it makes sense that brands pay in aggregate ~$175 billion in search ad revenue to drive traffic to their site.

But if a Google AI Overview or ChatGPT agent browses on the user’s behalf and returns the answer, why would the human continue onto the brand websites? this is the dramatic threat. Sama says they’re now handling a staggering 2.5 billion prompts every day, with 330 million daily queries coming from the U.S. alone. This is 1/6th of google’s volume. 8 months ago that figure was <1B … what rate will this continue to grow at?

in the future there is no reason for the customer to continue onto the website once theyve retrieved their answer. this is the catalyst for the implosion.

we are getting the answer and then moving on.

is this inevitable? what is required to enable this? what does it mean for the future of commerce, advertising and user experiences? Is there a generational startup opportunity? I’m not sure, but I’d like to find out.

history

In the beginning there was nothing. big primordial void. im gonna skip ahead a couple years past the grunting apes to when we codified a set of sounds to represent observed objects and experiences. Functionally, we were communicating (transferring) information: nearby danger, territorial claims, etc. This happened mostly orally, with some hand waving and a lot of bonking.

To no ones modern surprise, the scalability of conveying information to the entire population orally is infeasible within a life time. some bloke was fed up with managing record keeping through a game of telephone and decided to write onto a slab of rock the Kish tablet. Writing is important because it unlocked the rate at which information could be consumed. 2(+) people could read it at the same time. at any point in the day. without blud even being there. plus the information was (literally) set in stone - no one could mishear things.

However, writing itself had a bottleneck: duplication. To reach a wider audience, written material had to be manually copied or moved, which limited the dissemination of ideas. for a couple thousand years, ppl would just show up to the town square or have many scribes reproduce the works - no wonder so many religious monks had commentaries on the commentaries. The invention of the printing press unlocked duplication by stamping the same pages over and over. This is particularly important because (until 1440 - tho china figured it out in the 800s) only powerful institutions with the manpower could disseminate (and contril) ideas. to no ones postmodern surprise, the second major use of the printing press was porn.

Ok now we got consumable information, duplicatable at close to 0 marginal cost. the next bottleneck was

distribution: getting written information into the hands of the public was still a complex task. steam-powered printing presses drastically reduced the cost of printing and enabled newspapers to produce large volumes of copies at a lower price. The “Relation aller Fürnemmen und gedenckwürdigen Historien” in Germany, and the “Gazette” in France, provided regular updates on news, events and information to the masses.

The bottleneck of distribution gradually got less restrictive until the internet made distribution virtually free and accessible to everyone. Additionally, it was global. There were no physical or geographical limitations anymore. This is a major crux of this manifesto: infinite distribution + commoditization = personalization.

Before we go any further, there is an important milestone that I jumped over. Between the written mediums of newspapers and the internet, there existed (still exists?) the proliferation of ideas and information through radio and television. This is very very noteworthy because (for the first time outside of church) we would hear (and eventually see) information directly from its source, immediately. no next day paper. now.

There still remains two challenge: the creation and substantiation of ideas. while I can have numerous ideas and the Internet allows me to distribute them globally, I still need to write them down, just as artists need to create images and musicians need to compose songs. It is becoming increasingly evident that this bottleneck is also on the brink of being eliminated. Ill get to this later, but tldr: AI.

the history of ads

One of the earliest known ads was found in Thebes, Egypt, promoting a reward to capture and return a runaway slave named Shem. Since then, we have paid a very heavy price.

During the 1500s, print ads mainly focused on promoting events, plays, concerts, and products like books and medicines.

The first newspaper advertisement was published on April 17, 1704, in the Boston News-Letter, promoting an estate for sale. In 1741,

none other than the face of the $100 bill himself, pioneered magazine advertising in his ‘General Magazine’ booklet. Ben, frankly, this was a founding moment. In 1835, the very first billboard advertisement was created by Jared Bell in New York to promote Barnum & Bailey Circus.tbt to when zoos were cool and exotic

In 1841, Volney B. Palmer, the first ad agency, was established in Philadelphia. Instead of having to sell ads and build relationships with multiple newspapers, advertisers could work with the ad agency, which could leverage its connections with all those newspapers and serve multiple clients.

Radio gained significant popularity during and after World War II, but the first paid radio ad aired on August 22, 1922, on the New York City radio station, WEAF. The 15-minute ad, paid for by a real estate company called the Queensboro Corporation, promoted apartments in Jackson Heights, Queens. Later, the first television commercial aired in 1941 by the Bulova Watch Company. You can watch it here. It was ten seconds long and viewed by ~4,000 people in New York (#viral?).

The usefulness of ad agencies only grew as more advertising formats like radio and TV emerged. Particularly with TV, advertisers not only needed to place ads but also required significant help in creating them; ad agencies invested in ad-making expertise because they could apply this expertise across multiple clients. This led to the Golden Age of Advertising, where businesses made substantial investments in advertising to convey their brand’s uniqueness and engage their target audience.

Simultaneously, advertisers were rapidly expanding their geographic reach, especially after the Second World War; naturally, ad agencies expanded their reach as well, often through mergers and acquisitions. The primary business opportunity remained the same: provide advertisers with a one-stop shop for all their advertising needs.

Years later, after the development of ARPANET (1960s) and the World Wide Web (1989), the first online display ad was created in 1994 by AT&T, which asked users, “Have you ever clicked your mouse right HERE?” with an arrow pointing to text that read “YOU WILL.” The ad achieved a click-through rate of 44% - a figure that would astonish modern-day marketers. Fitting that the first ad was clickbait.

but why do ads actually work???

When the Internet came along, with its infinite distribution to infinite users, the newspapers, brands, and ad agencies were pumped af: more users = more money! Ad agencies in particular were frothing as more channels means more complexity and the ad agencies could abstract that away for their clients!

Before the Internet, a newspaper like the New York Times was limited in reach; now it can reach anyone on the planet! The problem for publishers, though, is that the free distribution provided by the Internet is not an exclusive. It’s available to every other newspaper as well. Moreover, it’s also available to publishers of any type. In the early internet (and to this day) individuals could post their own news updates, and to the indifferent HTML protocol, it was on ‘completely equal footing’.

That abundance of publications (blogs, webpages, brandsites, etc) meant that discovery was far more important than distribution.

So, two kids in a garage in palo alto decide to invent a way to rank pages, aptly called PageRank. Actually, much like the printing press, the groundwork was done in china. The first successful strategy for site-scoring and page-ranking was link analysis: ranking the popularity of a web site based on how many other sites had linked to it. Robert Li’s RankDex was created in 1996, filed for patent in 1997, granted in 1999, and then he used it to found Baidu in 2000. Larry Page referenced Robin Li’s work in the citations for PageRank.

Increasingly users congregated on two discovery platforms: Google for things for which they were actively looking, and Facebook for entertainment.

IRL

Start with the top 25 advertisers in the U.S. The list is made up of:

4 telecom companies (AT&T, Comcast, Verizon, Softbank/Sprint)

4 automobile companies (General Motors, Ford, Fiat Chrysler, Toyota)

4 credit card companies (America Express, JPMorgan Chase, Bank of America, Capital One)

3 consumer packaged goods (CPG) companies (Procter & Gamble, L’Oréal, Johnson & Johnson)

3 entertainment companies (Disney, Time Warner, 21st Century Fox)

3 retailers (Walmart, Target, Macy’s)

1 from electronics (Samsung), pharmaceuticals (Pfizer), and beer (Anheuser-Busch InBev)

Before going into Google and Facebook’s operating models more deeply, lets look to a more simple analog example. Buying the swiffer (Procter & Gamble’s cleaning mop stick thingy) in a Target. why do we decide to do so?

Ad agencies would say it is due to successful guidance through the Purchase Funnel, a concept initially introduced in 1925 in Edward Strong’s book, The Psychology of Selling and Advertising. The funnel is composed of: “attention, interest, desire, action, satisfaction”.

The real credit goes to E. St. Elmo Lewis, who in 1898 introduced the slogan, “Attract attention, maintain interest, create desire,” during an advertising course he taught in Philadelphia. He mentioned that he derived the idea from studying the psychology of William James. Later, he expanded the formula to include “get action.” Around 1907, A.F. Sheldon further enhanced it by adding “permanent satisfaction” as a crucial element. Although few in 1907 recognized the importance of this last phrase, today it is widely acknowledged as essential for providing service, gaining the buyer’s goodwill, meeting their needs, and ensuring lasting satisfaction.

Anyway,

- Attention: make the buyer aware of a problem they have

- Interest: the buyer becomes interested in solving their problem

- Desire: the buyer becomes interested in your solution to their problem

- Action: the buyer acquires your solution

A classic example of the complete AIDA model condensed into a single commercial is this roll-out campaign for the Swiffer mop

The entire funnel is encapsulated in this ad:

- Attention: Traditional cleaning methods stir up dirt

- Interest: Dirt needs to be removed, not just moved

- Desire: Swiffer cloths collect dirt and can be thrown away

- Action: Find Swiffer in the household cleaning aisle

The reference to the aisle is crucial: shelf space has long been the cornerstone for large consumer packaged goods companies. Swiffer achieved widespread distribution immediately upon launch because P&G could leverage its other popular products during negotiations with retailers like Walmart and Target to secure the best shelf location placement. Importantly, simply being on shelves increases the likelihood that customers will discover you independently or recognize you after repeated exposure. in ‘traditional retail advertising’ shelf space provided both distribution and discovery.

Notice that the vast majority of the industries on the list are dominated by massive companies that compete on scale and distribution. CPG is the perfect example: building a “house of brands” allows a company like Procter & Gamble to leverage scale to invest in R&D, reduce the cost of products, and target demographic groups without perfect personalization. TV is the perfect medium to cater to the masses. In fact, the top 200 advertisers in the U.S love TV so much that they make up 80% of television advertising, despite accounting for only 51% of total advertising spend (and 41% of digital).

Linear television and its advertisers were fundamentally based on controlling distribution (i.e. retail shelf space) and thereby controlling customers.

Many of the companies on this list are now under threat from the Internet. When supply was limited by physical space, shelves were highly valuable for both discovery and distribution. But with the Internet making shelf space virtually limitless, these brands can no longer monopolize the once-scarce shelf space. and I’m no mathematician, but it’s clear that trying to dominate an infinite space is a losing battle. Specifically:

- CPG companies face threats on two fronts: on the high end, the combination of e-commerce and highly-targeted, highly-measurable Facebook advertising has led to a rise in boutique CPG brands offering superior products to very specific groups. On the low end, e-commerce not only diminishes the shelf-space advantage but also sees Amazon making significant moves into private label products.

- Similarly, big box retailers that offer little beyond availability and low prices are being surpassed by Amazon in both areas. In the long term, it’s difficult to see how they will continue to survive.

- Automobile companies, on the other hand, are dealing with three distinct challenges: electrification, transportation-as-a-service (like Uber), and self-driving cars. The latter two, in particular (and to some extent the first), suggest a future where cars become mere commodities purchased by fleets, making advertising to customers obsolete.

Many of these major companies, consciously, unconsciously, or under the veil of ‘Hate Speech’, decided to boycott Facebook in 2020. Household brands like Coca-Cola, J.M. Smucker Company, Diageo, Mars, HP, CVS Health, Clorox, Microsoft, Procter & Gamble, Samsung, Walmart, Geico, Hershey and 1000 others decided to pull their spending on the app. Seems like a major blow, right? Zuckerberg was unphased.

For reference, 2019 Facebook’s top 100 advertisers made up less than 6% of the company’s ad revenue. Most of the $69.7 billion the company brought in came from its long tail of 8 million advertisers. This explains why the news about large CPG companies boycotting Facebook is, from a financial perspective, simply not a big deal.

Unilever’s measly $11.8 million in U.S. ad spend, to take one example, is replaced with the same automated efficiency that Facebook’s timeline ensures you never run out of content. Facebook loses some top-line revenue – in an auction-based system, less demand corresponds to lower prices. And yet, due to these lower prices, smaller direct-to-consumer companies can now bid and steal customers from massive conglomerates like Unilever. The content will be filled regardless, and the markets are very efficient.

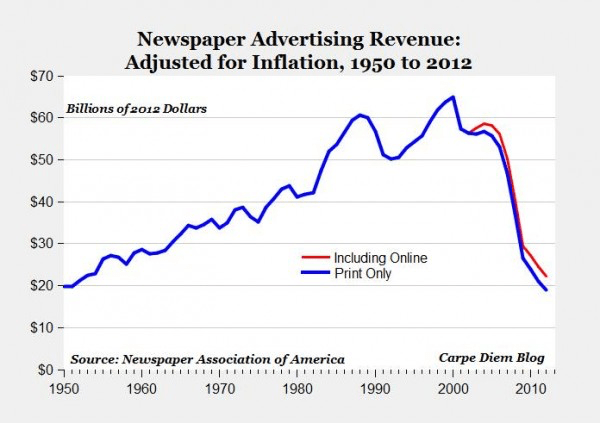

The unavoidable truth is that TV advertisers are 20th-century entities: designed for mass markets, not niches, designed for brick-and-mortar retailers, not e-commerce. These companies were built on TV, and TV was built on their advertisements. While they are currently supporting each other, the decline of one will accelerate the decline of the other. For now, the interdependence of these models is keeping them afloat, but it only means that when the end comes, it will arrive more quickly and broadly than anyone anticipates.

Online

the traditional marketing funnel made sense in a world where different parts of the customer journey happened in different places — literally. You might see an advertisement on TV, then a coupon in the newspaper, and finally the product on an end cap in a store. Every one of those exposures was a discrete advertising event that culminated in the customer picking up the product in question in putting it in their (literal) shopping cart.

One of the hallmarks of the Internet is that the entire AIDA funnel can be often compressed into a single Facebook ad that you might only see for a fraction of a second; perhaps something will catch your eye, and you will swipe to see more, and if you are intrigued, you can complete the purchase right then and there. The journey is increasingly compressed into a single impression: you see an ad on Instagram, you click on it to find out more, you login with Shop Pay, and then you wonder what you were thinking when it shows up at your door a few days later. The loop for apps is even tighter: you see an ad, click an ‘Install’ button, and are playing a level just seconds later. Sure, there are things like re-targeting or list building, but by-and-large Internet advertising, particularly when it comes to Facebook, is almost all direct response. You might even forget about your purchase right up until a mysterious package shows up at your door a few days later.

Due to the format of these ads, digital advertising has worked much better for direct response marketing. Aka impulse purchases. Notice how this is a very different commerce behavior than having gone to Target, motivated by a TV ad + newspaper coupon, to examine the physical usefulness. Now:

- Facebook helps find the customers

- Shopify or WooCommerce build the storefronts

- Stripe or PayPal handle payments

- Third-party logistics providers package and ship the goods

- USPS, Fedex, and UPS deliver the actual packages

In the same way that the internet made the distribution and duplication of content indiscriminantly, facebook ads allows anyone to put an ad that can reach anyone. This has the same effect of creating perfect competition.

Here is the problem for DTC commerce: Facebook really is better at finding brands’ customers than anyone else. This alludes to Zuck’s endgame, but essentialy DTC ad budgets are forced onto facebook as it is the best (measured) return-on-investment for acquired customers on Facebook, where DTC companies are competing against all of the other DTC companies and mobile game developers and incumbent CPG companies and everyone else for user attention. That means the real winner is Facebook, while DTC companies are slowly choked by ever-increasing customer acquisition costs. Facebook is the company that makes the space work, and so it is only natural that Facebook is harvesting most of the profitability from the DTC value chain.

What made the Facebook model work is that the Meta Pixel (now CAPIs) could map a conversion (downloading of an app/purchasing the swiffer) to ad-targeted customers on their social media app. because Facebook knew a lot about someone who saw each ad and thereafter converted, they created an algorithm in 2013 that could easily find other people who were similar and show them similar ads (lookalike audiences). Along with the news feed, this was one of the biggest moments in Facebook’s history. From then on, they could use the data flywheel to continually optimizing their targeting and increasing their understanding along the way. Now Advantage+ is essentially a 1-click “set it and forget it”.

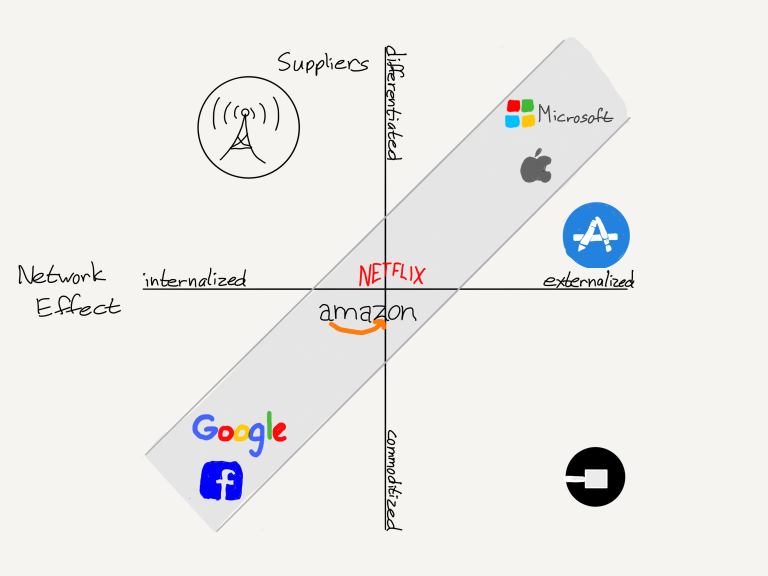

This has fundamentally changed the plane of competition: no longer do distributors compete based upon exclusive supplier relationships, with consumers/users an afterthought. Instead, suppliers can be commoditized leaving consumers/users as a first order priority. By extension, this means that the most important factor determining success is the user experience: the best distributors/aggregators/market-makers win by providing the best experience, which earns them the most consumers/users, which attracts the most suppliers, which enhances the user experience in a virtuous cycle.

Ben Thompson, Aggregation Theory (2015)

To be fair to the DTC companies, they are hardly the first to make this mistake: when the internet newspapers looked at the Internet and only saw the potential of reaching new customers; they didn’t consider that because every other publisher in the world could now reach those exact same customers, the integration that drove their business — publishing and distribution in a unique geographic area — had disintegrated. For a (long) time, Newspapers dominated both editorial and advertisements, but it turns out that was simply a function of who owned printing presses and delivery trucks; once the Internet came along advertisers, which cared about reaching customers, not supporting journalists, switched to Facebook and Google, which had aggregated the former and commoditized the latter. It is the same lesson that TV-era brands are facing now that they can’t just win by dominating shelf space. If some part of the value chain becomes free, that is not simply an opportunity but also a warning that the entire value chain is going to be transformed. How will brands adapt?

https://stratechery.com/2020/email-addresses-and-razor-blades/

Facebook, Amazon, Netflix, and Google (plus Uber/Airbnb etc) are structurally very similar companies: all leveraged zero distribution costs and zero transaction costs to own users at scale via a superior experience that commoditized suppliers and let them skim off the middle, either through fees, subscriptions, and/or ads.

Google, though, has a built-in advantage: Google doesn’t have to figure out what you are interested in because you do the company the favor of telling it by searching for it. The odds that you want a hotel in San Francisco are rather high if you search for “San Francisco hotels”; it’s the same thing with life insurance or car mechanics or e-commerce.

Amazon goes a step further and has effectively integrated the entire e-commerce stack when it comes to the distribution of goods consumers are explicitly searching for:

- Customers come to Amazon directly

- Searches on Amazon lead to Amazon product pages or 3rd-party merchant listings that look identical to Amazon product pages

- Amazon handles payments

- Amazon packages and ships the goods

- Amazon increasingly delivers the actual packages

This is great for aggregators like Google and Amazon, but not so great for P&G: remember, dominating shelf space was a core part of their strategy, and Amazon and Google have infinite shelf space! Anyone can publish, and this creates perfect competition - terrible for suppliers who face commoditization and shrinking margins, but great for consumers who enjoy more choices and lower prices.

gaming the algorithms

There are two big challenges when it comes to winning search:

- Because search is initiated by the customer, you want that customer to not just recognize your brand (which is all that is necessary in a physical store), but to also recall your brand (and enter it in the search box). This is a much stiffer challenge and makes the amount of time and money you need to spend on a brand that much greater.

- If prospective customers do not search for your brand name but instead search for a generic term like “laundry detergent” then you need to be at the top of the search results. And, the best way to be at the top is to be the best-seller. In other words, having lots of products in the same space can work against you because you are diluting your own sales and thus hurting your search results.

In order to survive on the Internet, an ugly truth was emerging. One has to cater to Google. They have all the customers. Yelp and countless other sites depend on Google to bring them web traffic — eyeballs for their advertisers.

Yelp, like many other review sites, has deep roots in SEO — search-engine optimization. Their entire business was long predicated on Google doing their customer acquisition for them. This meant a heavy emphasis on both speed and SEO, and an investment in anticipating and creating content to answer consumer questions. This includes using tools like SemRush and hiring SEO-specialized ad agencies to flourish online. And to their credit, since their founding in 2004, they’ve had great success in being the destination website for restaurant reviews and the sort.

You may think, are does anything even change if you play the SEO game? The answer is a big-time yes. Even a small boost at the scale at which google operates (13.7B searches/day, 5T/year), would be huge.

| Google Search Feature | Click Through Rate (CTR) |

|---|---|

| Ad Position 1 | 2.1% |

| Ad Position 2 | 1.4% |

| Ad Position 3 | 1.3% |

| Ad Position 4 | 1.1% |

| Search Position 1 | 39.8 § |

| Search Position 2 | 18.7% §§ |

| Search Position 3 | 10.2% |

| Search Position 4 | 7.2% |

| Search Position 5 | 5.1% |

| Search Position 6 | 4.4% |

| Search Position 7 | 3.0% |

| Search Position 8 | 2.1% |

| Search Position 9 | 1.9% |

| Search Position 10 | 1.6% |

- § If snippet, then 42.9%; If AI overview, then 38.9%; If local pack present, then 23.7%

- §§ If snippet, then 27.4%; If AI overview, then 29.5%; If local pack present, then 15.1%

Source: First Page Sage

But the data is more than just a small boost - the jump from 18.7% to 27.4% CTR is massive. For most companies, going from search position 8 to search position 3 (or vice versa) can make or break a business.

But AI Overviews (AIO) are existential threats to companies like Yelp. Look at what Chegg wrote in their 2024 Annual Financial Report:

While we made significant headway on our technology, product, and marketing programs, 2024 came with a series of challenges, including the rapid evolution of the content landscape, particularly the rise of Google AIO, which as I previously mentioned, has had a profound impact on Chegg’s traffic, revenue, and workforce. As already mentioned, we are filing a complaint against Google LLC and Alphabet Inc. in the U.S. District Court for the District of Columbia, making three main arguments. We allege in our complaint, Google AIO has transformed Google from a “search engine” into an “answer engine,” displaying AI-generated content sourced from third-party sites like Chegg. Google’s expansion of AIO forces traffic to remain on Google, eliminating the need to go to third-party content source sites. The impact on Chegg’s business is clear. Our non-subscriber traffic plummeted to negative 49% in January 2025, down significantly from the modest 8% decline we reported in Q2 2024.

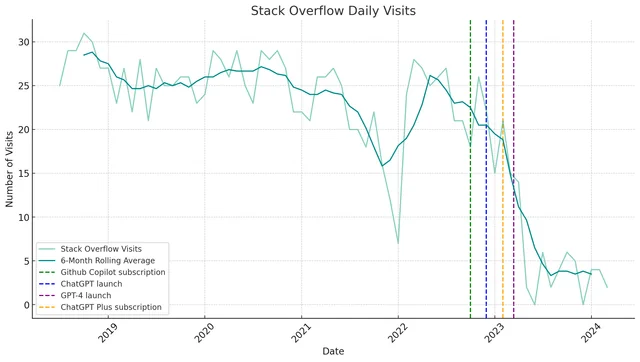

Theyre not the only one, Stack Overflow has taken a massive hit too. These companies relied on the handshake promise that google can use my content in return for traffic to my website where i can thereafter sell goods / services. Or at the very least display banner ads on their website.

In a 2014 video that Yelp put out, while it makes many of the same arguments as the Chegg lawsuit, instead of being focused on regulators it is targeting Google itself. They argue that Google isn’t living up to its own standards by not featuring the best results, and not driving traffic back to sites that make the content Google needs (by, for example, not including prominent links to the content filling its answer boxes; Yelp isn’t asking that they go away, just that they drive traffic to 3rd parties). Google may be an aggregator, but it still needs supply, which means it needs a sustainable open web.

Yelp, Chegg and Stack Overflow are not the first and not the last to be at the whims of Google. Back in 2006, Belgian news publishers sued Google over their inclusion in the Google News, demanding that Google remove them. After winning the initial suit, Google dropped them as demanded. Then the publications, watching their traffic drop dramatically, scrambled to get back in. That same year’s Field v. Google held that Google’s usage of snippets of the plaintiff’s content was fair use, and furthermore, that Blake Fields, the author, had implicitly given Google a license to cache his content by not specifying to Google to not crawl his website.

In 2014, A group of German publishers started legal action against the search giant, demanding 11 percent of all revenue stemming from pages that include listings from their sites. In the case of the Belgian publishers in particular, it was difficult to understand what they were trying to accomplish. After all, isn’t the goal more page views (it certainly was in the end!)? The German publishers in this case are being a little more creative: like the Belgians before them they are alleging that Google benefits from their content, but instead of risking their traffic by leaving Google, they’re instead demanding Google give them a cut of the revenue they feel they deserve.

The obvious reaction to this case, as with the Belgian one, is to marvel at the publisher’s nerve; after all, as we saw with the Belgians, Google is the one driving traffic from which the publishers profit. “Ganz im Gegenteil!” say the publishers. “Google would not exist without our content.” And, at a very high level, I suppose that’s true, but it’s true in a way that doesn’t matter, and understanding why it doesn’t matter gets at the core reason why traditional journalistic institutions are having so much trouble in the Internet era.

The ugly truth, though, as these newspaper publishers found out, is that not being in Google means a dramatic drop in traffic. No website can afford to exclude Google’s crawler from robots.txt because it would be economically ruinous. AI Overviews snippets in search (Google’s defense against AI-chatbot incursions into their search dominance) requires that if you want your content available to Google Search — and any publisher must — then your content will go into Google’s most important AI product as well.

Not everyone wants to play into Google’s game, though. Even when their ad business tanked 30% around the same time snippets were introduced, the New York Times wrote:

We are, in the simplest terms, a subscription-first business. Our focus on subscribers sets us apart in crucial ways from many other media organizations. We are not trying to maximize clicks and sell low-margin advertising against them. We are not trying to win a pageviews arms race. We believe that the more sound business strategy for The Times is to provide journalism so strong that several million people around the world are willing to pay for it. Of course, this strategy is also deeply in tune with our longtime values. Our incentives point us toward journalistic excellence … [yet] our journalism must change to match, and anticipate, the habits, needs and desires of our readers, present and future.

That raises the question as to what are the vectors on which “destination sites” — those that attract users directly, independent of the Aggregators — compete? The obvious two candidates are focus and quality. What is important to note, though, is that while quality is relatively binary, the number of ways to be focused — that is, the number of niches in the world — are effectively infinite; success, in other words, is about delivering superior quality in your niche — the former is defined by the latter.

The transformative impact of the Internet is only starting to be felt, which is to say that the long run will be less about traditional companies adopting digital than it will be about their entire way of doing business being rendered obsolete.

why now

It was a symbiotic relationship. Google benefited from being on THE place to find information. Users benefited by quickly finding what they needed. Websites and content creators benefited with larger audiences, focused and happy users, and a clear-cut path toward success. We all got what we needed out of the relationship.

Source: brob

As long as Google was providing ten blue links, it could serve everyone, no matter their values; after all, the user decided which link to click.

By providing ads alongside those ten blue links, Google deputized the end user to choose the winner of the auction it conducted amongst advertisers; those advertisers would pay a premium to win that auction because their potential customer was affirmatively choosing to go to their site, which meant (1) a higher chance of conversion and (2) the possibility of building a long-term relationship to increase lifetime value.

AI threatens this:

If a user doesn’t have to choose from search results, said user also doesn’t have the opportunity to click an ad, thus choosing the winner of the competition Google created between its advertisers for user attention. Because AI gives an answer instead of links, there is no organic place to put the advertisements, bid in its 4 SERP auctions. It is not that Google is artificially constraining its horizontal business model; it is that its business model is being constrained by the reality of a world where, as Pichai noted, artificial intelligence comes first.

In the world of AI Agents you must own the interaction point, and unfortunately there is no room for ads, rendering both Google’s distribution and business model moot. For Google, both must change for the company’s technological advantage to come to the fore.

Ben Thompson, India and Gemini: Ten Blue Links & The Complicity Framework (2024)

Additionally, when AI reduces the 10 blue links to one answer, if the subject rests on subjective values, the search result can never satisfy everyone, Google risks upsetting a significant portion of demand, weakening its Aggregator position and potentially decreasing its leverage on costs. For example, a WIRED analysis demonstrated that:

despite claims that Perplexity’s tools provide “instant, reliable answers to any question with complete sources and citations included,” doing away with the need to “click on different links,” its chatbot, which is capable of accurately summarizing journalistic work with appropriate credit, is also prone to bullshitting, in the technical sense of the word.

This undermines the trustworthiness of the AI Overview, and thus also information the end user consumes (and could therafter recite).

There are three major open threads here (opportunities?), which we’ll go into more in depth in the sections on AI Web, Human Interfacing and Economic Incentives.

what now?

What exactly is happening rn in search?

Sundar Pichai when asked about search volume in their 2024 Q4 Earnings Call:

On Search usage overall, our metrics are healthy. We are continuing to see growth in Search on a year-on-year basis in terms of overall usage. Of course, within that, AI overviews has seen stronger growth, particularly across all segments of users, including in younger users. So it’s being well received. But overall, I think through this AI moment, I think Search is continuing to perform well. And as I said earlier, we have a lot more innovations to come this year. I think the product will evolve even more. And I think as you make Search, as you give, as you make it more easy for people to interact and ask follow-up questions, et cetera, I think we have an opportunity to drive further growth. Our Products and Platforms put AI into the hands of billions of people around the world. We have seven Products and Platforms with over 2 billion users and all are using Gemini. That includes Search, where Gemini is powering our AI overviews. People use Search more with AI overviews and usage growth increases over time as people learn that they can ask new types of questions. This behavior is even more pronounced with younger users who really appreciate the speed and efficiency of this new format.

This echoes the “we built Google for users, not websites” Eric Schmidt ethos that Google generally adheres to. In Q1 2025 Pichai writes that they have 1.5B monthly active users using AI Overviews.

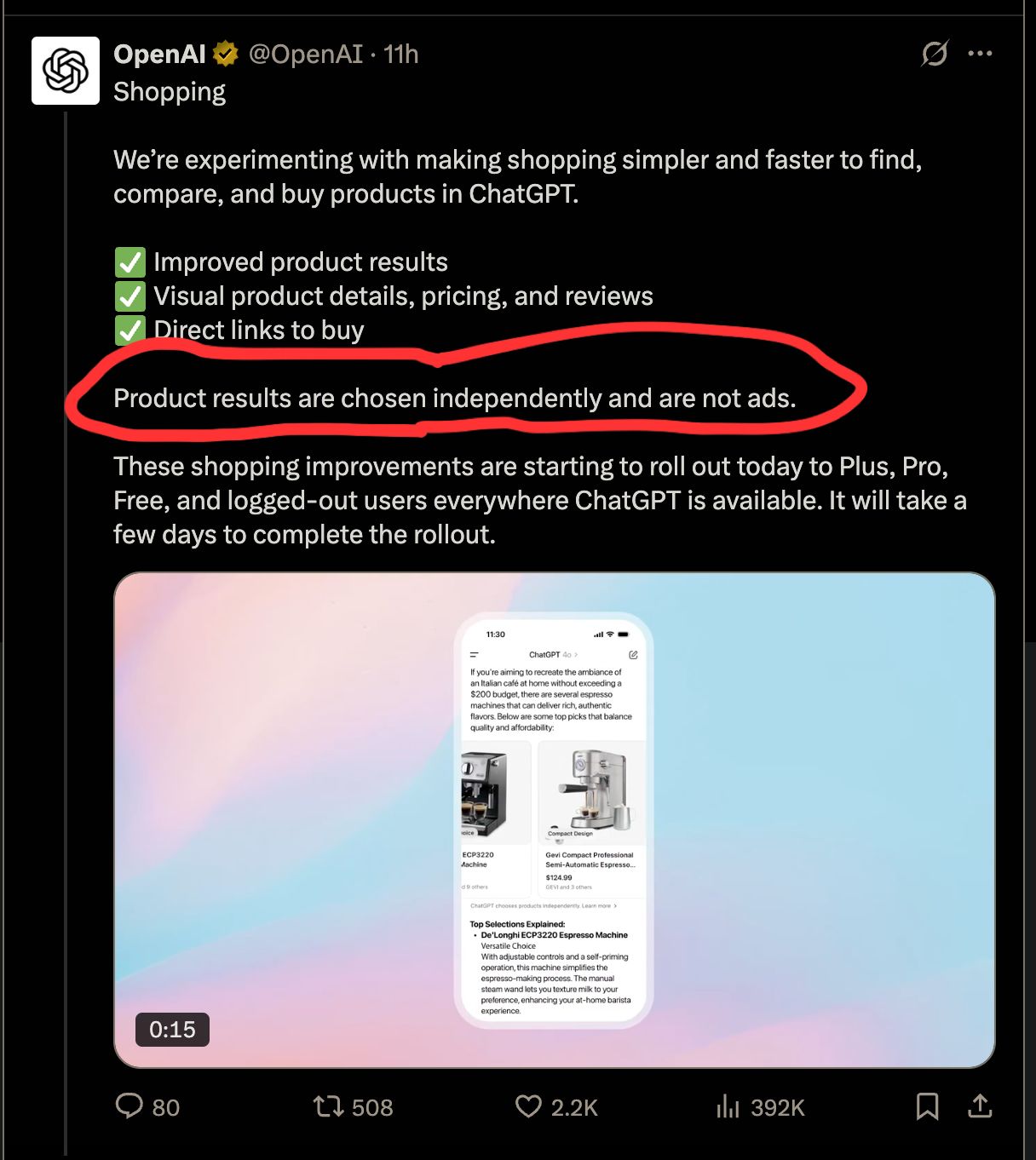

Ok so if there are no places to put Search Enging Result Page (SERP) ads anymore, but does that mean there’s no place to put ads at all? Of course not.

In the Perplexity pitch deck, Perplexity explains how their ads would show up as a side banner or a sponsored ‘follow up link’. In October, Google rolled out displaying ads alongside the AI answer (also see last week’s launch of NexAD for smaller AI search engines), much like what Perplexity pioneered a few months earlier. CBO Philipp Schindler reports positive results for AI search overview advertising:

First of all, AI overviews, which is really nice to see, continue to drive higher satisfaction and search usage. So, that’s really good. And as you know, we recently launched the ads within AI overviews on mobile in the U.S., which builds on our previous rollout of ads above and below. And as I talked about before, for the AI overviews overall, we actually see monetization at approximately the same rate, which I think really gives us a strong base on which we can innovate even more.

“We do have very good ideas for native ad concepts but you’ll see us lead with user experience…just like you’ve seen with YouTube, we’ll give people options over time, but for this year I think you’ll see us be focused on the subscription.” - pichai

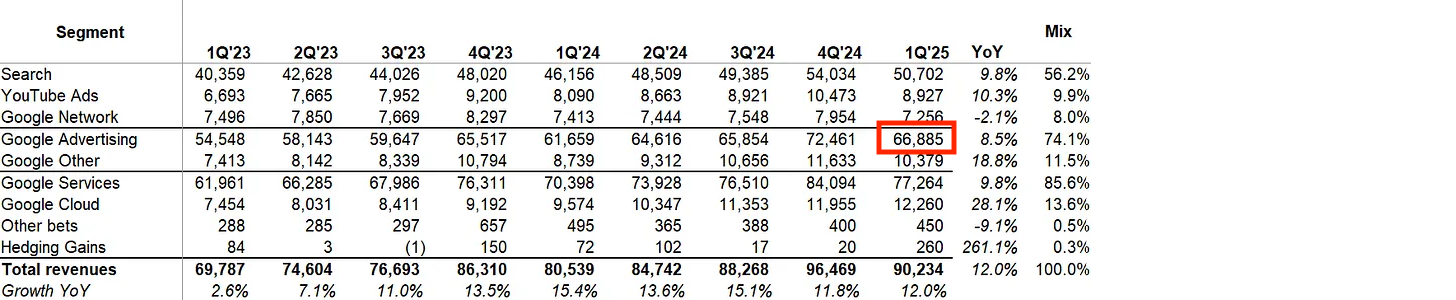

Figure: Source: Alphabet Filings, MBI.*

Although this is true, there is is some obfuscation to this truth. We can see that after the gradual rollout of AIO in Q4, Q1 reigned in $66,886M “approximately the same” as last year’s 61,659M. This is notably much less, though. An 8.47% YoY Growth is similar, sure, but also strictly worse than the previous year’s (61659÷54548) 13.03%.

Not only is it worse, but they’re hiding something very important - Cost Per Click has been increasing quite a bit. They cant do this forever.

Unfortunately, these are temporary fixes to a much larger problem.

Problem 1: human interfacing

Figure: Source: Alphabet Filings, MBI.*

Its one thing to replace human agencnies. Its another to replace human agency.

Yes, many of these ad agencies are built on helping brands like Proctor & Gamble find and market to their customers. Since the inception of the advertisement the goal has been to nudge customers to grow an affinity to and purchase their goods and services. Ads encourage the Attention, Interest, Desire and/or Action of purchasing behavior.

Search ads have always been a great place for advertisement because they catch users at a high intent moment. Meaning, a user is actively looking for something, and if you can provide the solution (according to their taste), theyll pick you!

One of the benefits of having 10 blue links was the choice. Users could be the arbiter of taste. Ads and SEO optimized links were entered into the arena of usefulness and the user could declare the victor. This was particularly relevant for Google, who could use a human’s click as a ranking parameter. Now, when an AI Overview is spitting out the answer, the search engine is the arbiter of taste.

This is problematic for two major reasons: Trustworthiness and Usefulness.

Trustworthiness

Google wants to “make information universally accessible and useful”. So, over the years, they’ve tried a bunch of stuff:

Each feature launch was an incremental improvement for Google’s search users. Search for a local restaurant, get a widget in the sidebar (nice and out of the way) with important information like the phone number, address, and even a link to the website. Nice!

All these changes make sense from the Google Side - Google ads became more important (and thus user engagement became more important), so Google wanted fewer users leaving the search page.

Seeing a 2 on the screen when a consumer enters 1+1 is handy, but it’s not without cost. If someone runs a calculator website, showing the 2 could lead to the calculator website’s traffic decline. Google must, therefore, make tradeoffs. These tradeoffs typically are good for users, but not always. As Eric Schmidt once said, “we built Google for users, not websites.” That’s reasonable, especially when it comes to immutable facts. Giving billions of users a quick answer to 1+1 seems like it outweighs the cost of lost traffic to the calculator website operator. But who decides that?

And what if its not true?!

Yes that seems silly to say when the quick snippet answer to 1+1= spits out 2, everyone can indeed agree it is truthful (fun fact it took Bertrand Russell and Alfred North Whitehead 300+ pages to prove this). But what if the “answer” being served up is best pediatrician mountain view ca?

Google will give you an answer: 10 blue links that point capture 99.37% of clicks. meaning, if you’re not in the top 10 ranked pediatricians, you wont get any business. And so SEO optimization games begin for attention capture and algorithmic blessing. These aren’t actually the best pediatricians in mountain view - theyre the best SEO optimized pediatricians in mountainview. This is untrustworthy in itself sure, but AI Overviews take this to another level because it draws from the gamified blue links and its own intuited world model.

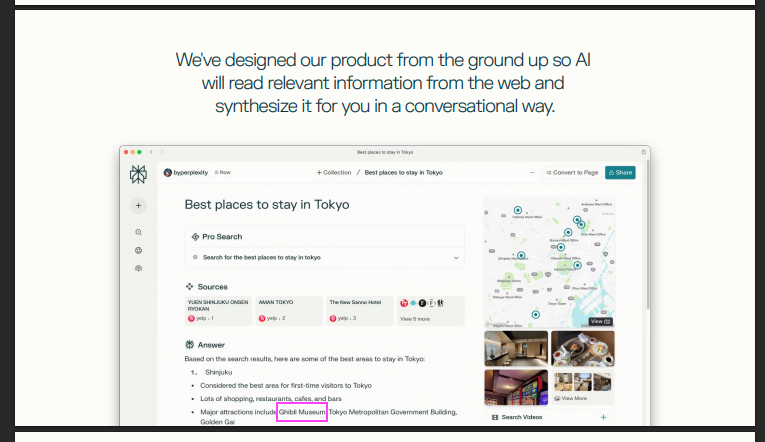

When Google’s AIO came out, there was a HUGE problem with the trustworthiness of its answers. It would suggest putting glue on pizza to stop the cheese from sliding, smoking 2-3 cigarretes/day while pregnant and that it indeed violates antitrust law (wait that one actually might be true). See a funny compilation here. Even within their own official pitch deck, Perplexity’s AI answer includes a hallucination – the Studio Ghibli Museum isnt in Shinjuku, in fact, it isn’t even in Tokyo!

Figure: perplexity is a series Z company.

The web has a rich, competitive offering of services to help answer such a question, yet these search engines give themselves exclusive access to the prime real estate of the page, proclaiming ‘the best answer’ in its answer snippet. By doing this, user’s choices are being made for them. Your choice.

Are you worse off?

Its one thing to replace human agencnies. Its another to replace human agency.

Usefulness

One could argue that a 100% brand takeover is fine if its useful. Lets say you search for a hotel in shinjuku, and the hilton takes over. What percentage of people would just ‘go with it’, without further research? Taking it a step further, what if the there is a One Click 🪄✨ Button?

If your answer (/intuition) is any greater than the % that wouldve selected the same hotel after self discovery, we’ve lost agency, obviously. But usefulness? Harder to measure, but we can look at the counterfactual. If people search through the ten blue links until they find something they are content with, navigating all the levers (price, distance, availability, (subjective) quality, etc), and the distribution of purchases of hotels is any different than that with a brand takeover, it means that some people didnt get their first choice. They were nudged into a suboptimal choice. In my personal opinion, this is evil.

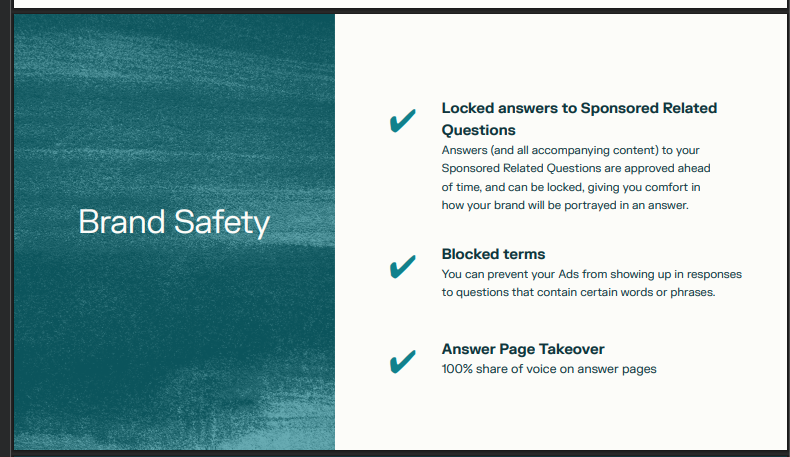

In April 2024, Chief Business Officer Dmitry Shevelenko told Digiday about the plans for a road map focused on “accuracy, speed and readability.” Shevelenko added that the company didn’t plan to rank sponsors differently than organic answers. “The weighting will be the same. That’s our version of ‘Don’t Do Evil,’” Shevelenko told Digiday earlier this year. “We’re not going to buy us an answer. Whenever we have advertising, that’s the one thing we don’t do: You can’t pay us to have the answer be different because you’re paying us.”

That certainly makes sense for Perplexity, which has one other important factor working in their favor: relative to Google, Perplexity doesn’t have any revenue to lose. ChatGPT similarly claims it wont let you ‘buy an answer’:

Figure: what happens when u usurp your core operating model.*

Yet its happening. Google announced a few days that it would pervasively display AIO ads. When does a banner ad taking up X% of the screen start having serious impacts on the freedom of choice? 1%->3%->10%->50%->100%? What about traffic to the websites?

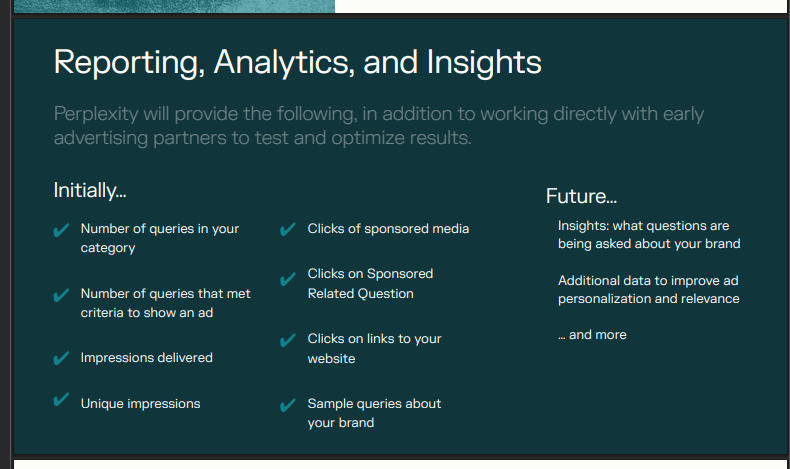

The first customers will be major brand advertisers who are both not necessarily looking for a click, but rather to build brand awareness and affinity, and who have infrastructure in place for measuring that (and, helpfully, they have experimental budgets that Perplexity can tap into for now). Brands that have strict brand guidelines, know what keywords to omit and have the bandwith to write manual ‘Sponsor Related Questions’. By blowing large budgets on AI Overviews, these Fortune 200s can not only build consumer Awareness and Interest, but buy Actions that wouldn’t have otherwise taken place. It shouldnt be a surprise either, that these companies are more price inelastic when the search engines increase CPC.

On their pitch deck, Perplexity boasts a 46% Follow-up Question rate. They highlight this because it is one of the opportunities for ad placement, where you can place a website that encourages discovery (e.g. ‘best running shoes -> best running shoes for a marathon’). But to me that screams ineffectiveness: 46% of the time, the user is coming to the platform and not getting the answer theyre looking for (sure, yes, some percentage is discovery, but not all of it). As mentioned before, this points to the ugly truth that for most questions, one search result can’t satisfy everyone. It just isnt useful enough.

Its important to reiterate that with a single answer, we not only reliquishing agency of our choices to The Big Five, but get a suboptimal answer meant to satisfy everyone. In an AI-first world where “we are getting the answer and then moving on,” the multi-visit discovery phase vanishes, collapsing the critical revenue stream for both Google and content publishers. These problems are dialed up to 11 when there are no longer any humans browsing.

Problem 2: ai web

Where we started

The World Wide Web (1989) was built by humans, for humans, and it started with written text, because of course, we started with written text for distribution to the masses. As people began hyperlinking to each other’s websites, the web quickly became cluttered and ‘unparsable for humans’. Don Norman, one of many researchers exploring how people interact with computers in the 1990s, coined “User Experience” (UX) - a shift from focusing solely on aesthetics and/or functionality to considering the user’s needs and emotions.

Google’s subsequent intervention (drawing on Robin Li’s work) was a welcomed relief, bringing us back to human-legible designs. As we know from earlier, they iterated quite a bit to make information universally accessible and useful.

But things changed when agents began browsing the web.

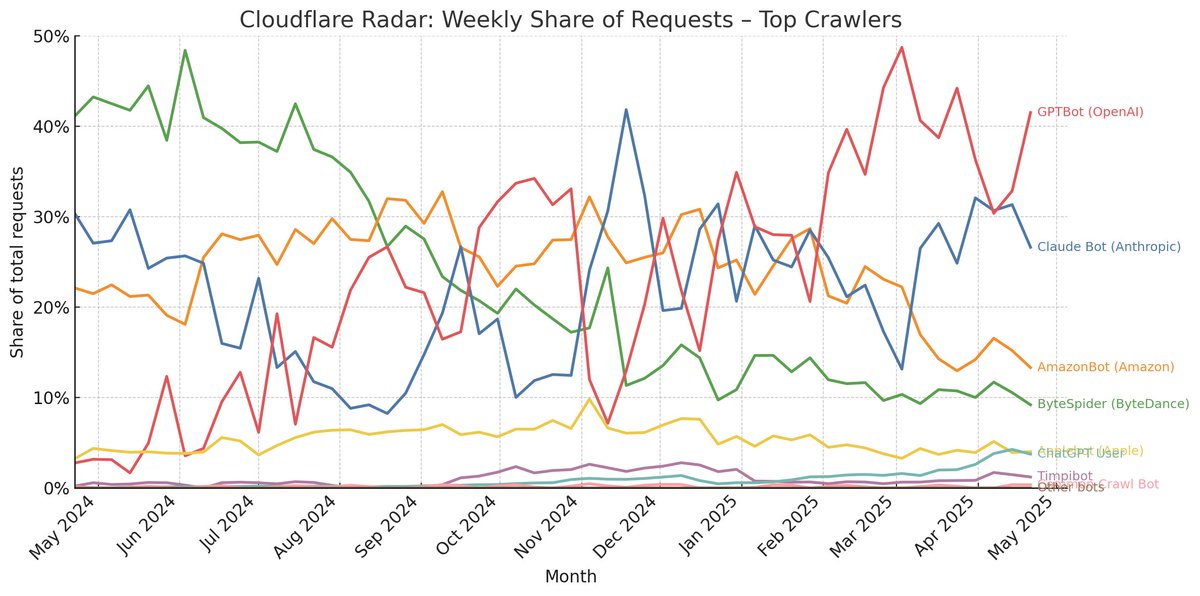

Figure: Source: Cloudflare Data Explorer

The Internet Archive announced back in 2017 that their crawler would ignore a widely accepted web standard known as the Robots Exclusion Protocol (robots.txt):

Over time we have observed that the robots.txt files that are geared toward search engine crawlers do not necessarily serve our archival purposes. Internet Archive’s goal is to create complete “snapshots” of web pages, including the duplicate content and the large versions of files. We have also seen an upsurge of the use of robots.txt files to remove entire domains from search engines when they transition from a live web site into a parked domain, which has historically also removed the entire domain from view in the Wayback Machine. In other words, a site goes out of business and then the parked domain is “blocked” from search engines and no one can look at the history of that site in the Wayback Machine anymore. We receive inquiries and complaints on these “disappeared” sites almost daily… We see the future of web archiving relying less on robots.txt file declarations geared toward search engines, and more on representing the web as it really was, and is, from a user’s perspective.

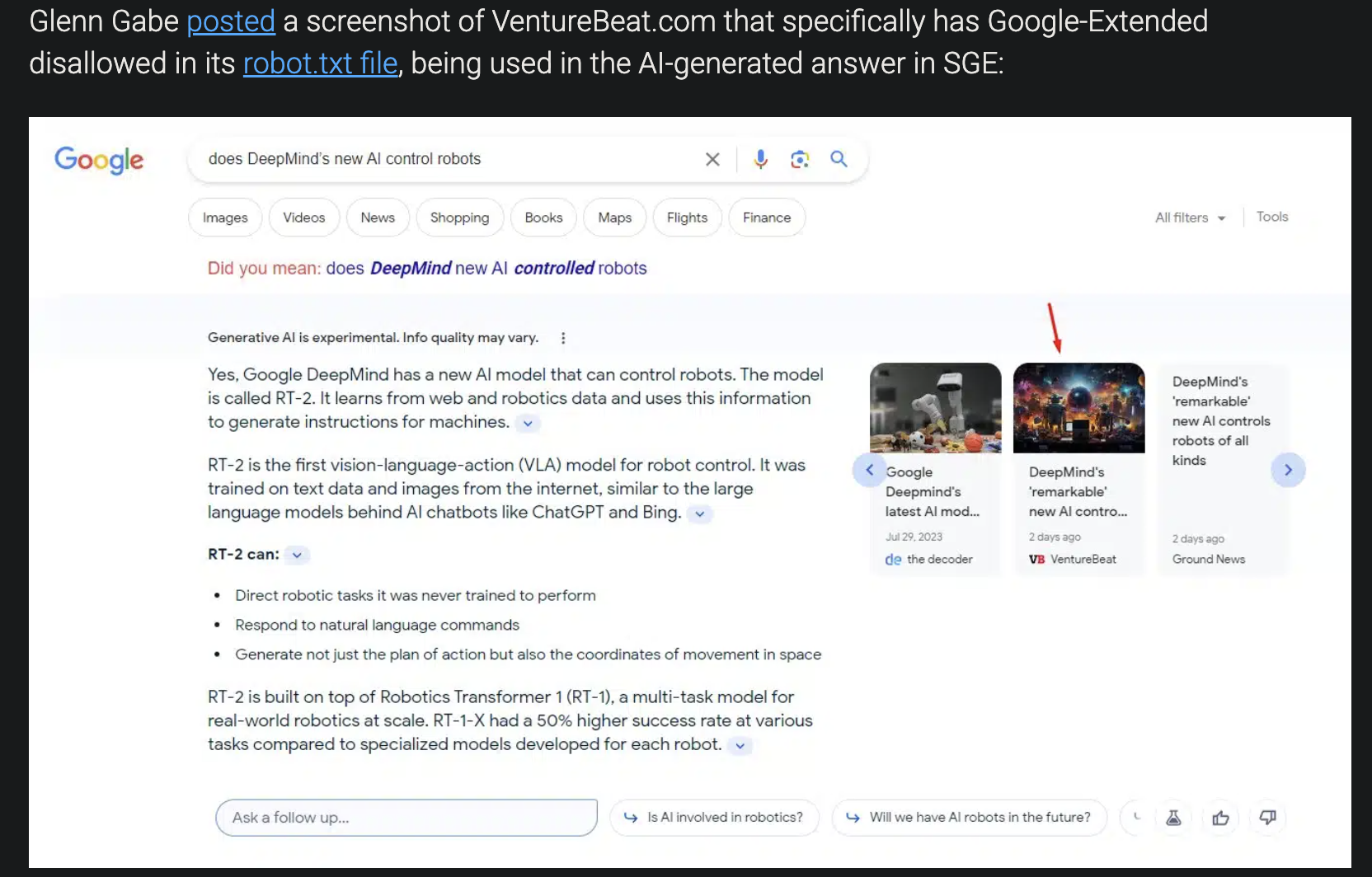

Maybe you can give them a pass, being a non-profit and all. But when these big AI companies started ignoring robots.txt, despite claiming that they don’t, things get complicated. Robb Knight at WIRED observed a machine — more specifically, one on an Amazon server and almost certainly operated by Perplexity — doing this on WIRED.com and across other Condé Nast publications. This, paired with clear regurgitations of NYT content by ChatGPT sparked a frenzy of lawsuits.

Figure: Source: The court case

OpenAI now lets you block its web crawler from scraping your site to help train GPT models. OpenAI said website operators can specifically disallow its GPTBot crawler on their site’s robots.txt file or block its IP address. “Web pages crawled with the GPTBot user agent may potentially be used to improve future models and are filtered to remove sources that require paywall access, are known to gather personally identifiable information (PII), or have text that violates our policies,” OpenAI said in the blog post. For sources that don’t fit the excluded criteria, “allowing GPTBot to access your site can help AI models become more accurate and improve their general capabilities and safety.”

Blocking the GPTBot may be the first step in OpenAI allowing internet users to opt out of having their data used for training its large language models. It follows some early attempts at creating a flag that would exclude content from training, like a “NoAI” tag conceived by DeviantArt last year. It does not retroactively remove content previously scraped from a site from ChatGPT’s training data.

Tbh this news isnt a solution. Call me cynical, but that last line explains why: OpenAI has already benefited from all of the data on the Internet, and established a norm that sites can opt out of future AI models, whicih cements the advantage of being a first mover and throws the ladder behind them. Since that announcement, GPTBot hasnt slowed down at all, as shown in the above image on crawlers. The opt out is nice, but its not like most publishers know how to update their robots.txt. Plus, who knows what economic impact of opting out these publishers would face.

its not like its stopping them from displaying the text in AIO either source

History seems to be rhyming with the German and Belgian publishers 20 years ago. Additionally, if these publishers are not increntivized, to continue giving content to these AIs, are we the stuck in the 2010s internet forever?

Keep in mind that it’s unclear that crawling Internet data is in any way illegal; I think there is a strong case that this sort of data collection is fair use, although the final determination of that question will be up to the courts (e.g., Shutterstock, NYT, Sarah Silverman vs OpenAI & friends). What is certain is that OpenAI isn’t giving the data it collected back.

Where we’re going

Beautiful Soup (bs4) and Selenium have been widely used for testing and automating interactions with web applications. These tools have been instrumental in allowing developers to extract data and simulate user interactions (e.g. what happens when you get the Reddit Hug of Death). 🅱️rowserBase took these tools and made them much more scalable and efficient by abstracting much of the complexity involved in setting up and managing browser instances via the cloud, allowing developers to focus on the logic of their automation tasks. One such task can be penetration testing, sure, but lately a new question is emerging.

What happens when AI agents start browsing on our behalf?

Take a moment to watch this agent buy their human a sandwich via 🅱️rowserbase’s headless browser:

Figure: Source: Evan Fenster on X the everything app

Notice how the AI never stopped or clicked on an ad. The agent had a task, and executed it.

This task was simple enough, as the order and supplier were explicit. But what happens when someone asks their AI Agent to “buy them a red sweater”? We’ll explore more of what the solution requires here, but lets focus on the ad problem in this section.

How should google count these impressions? If they stepped away to brew some coffee, would the user even know about any ads on the websites the agent browsed? Should they?

In a similar vein of questioning, Openai and Perplexity have ‘promised’ to never let you buy an answer, but what happens when the AI Overview / first link upon ‘red sweater’ search result is an ad? This very quickly rehashes the earlier problems of trustworthiness and usefulness.

Taking this a step further: remove the web browser interface altogether. Where are you going put the ads? In the GET requests between Shopify and Openai APIs?

There are a lot of questions here with no clear answers. However, their answers in the pre-Agentic Web era were the foundation on which attribution and discovery were fueled. These measurable ‘bounce rates’, ‘time on site’, etc were what Google, Meta, Shopify & friends used to measure the effectiveness and conversions of ads on their platform. Its all about to be uprooted with ‘personal agents’.

The decline of ads is approaching quicker than we think, first with the decline of publishers, and then with the decline of websites altogether.

Problem 3: the incentives

| Title | Link | Outcome |

|---|---|---|

| Ahrefs Study on CTR Decline | Google AI Overviews Hurt Click-Through Rates | 34.5% drop in CTR for top organic positions when AI Overviews are present. |

| Amsive Research on CTR Impact | Google AI Overviews Hurt Click-Through Rates | Average 15.49% CTR decline across 700,000 keywords; up to 37% drop for non-branded queries. |

| Raptive Estimate on Traffic and Revenue Loss | Why Publishers Fear Traffic Ad Declines from Google’s AI-Generated Search Results | AI Overviews could reduce publisher visits by up to 25%, leading to $2 billion in annual ad revenue losses. |

| Swipe Insight Report on Traffic Decline | Google’s AI Overviews Cause Publisher Traffic Decline Estimated $2B Ad Revenue Loss | Some publishers experienced up to a 60% decrease in organic search traffic due to AI Overviews. |

| World History Encyclopedia Case Study | AI Took My Readers: Inside a Publisher’s Traffic Collapse | Observed a 25% traffic drop after content appeared in AI Overviews. |

| WARC Study on CTR Reduction | AI Overviews Hit Publisher Traffic Hard, Study Finds | Organic click-through rates dropped to 0.6% when AI Overviews are present, compared to 17% for traditional links. |

| Bloomberg Report on Independent Websites | Google AI Search Shift Leaves Website Makers Feeling Betrayed | Independent websites have seen significant declines in traffic due to AI-generated answers. |

| eWeek Analysis on Web Traffic Decline | Google AI Overviews SMB Impact | Some website owners experienced up to a 70% decline in web traffic following AI Overviews introduction. |

| Northeastern University Insight | Google AI Search Engine | AI Overviews could reduce website traffic by about 25%, particularly affecting web publishers reliant on search traffic. |

| Press Gazette Warning on Publisher Visibility | Devastating Potential Impact of Google AI Overviews on Publisher Visibility Revealed | AI Overviews could dramatically impact publisher traffic and ad revenue, especially in health-related queries. |

The foundational handshake of the internet, where content creators exchange their material for traffic and potential revenue, is being shattered by AI overviews that eliminate the necessity for users to visit original content sites. The many studies above, as well as the many previously mentioned (Chegg, Stack Overflow and Yelp), highlight a 15-35% decline in click-through rates (CTR) when AI Overviews are present, with some publishers experiencing up to a 70% decrease in organic search traffic.

Publishers, once riding high on search engine traffic, are now staring down a harsh new reality: their content is being consumed without any direct interaction. Publishers are missing opportunities to sell their goods and services.

This isn’t just about losing ad revenue; it’s about survival.

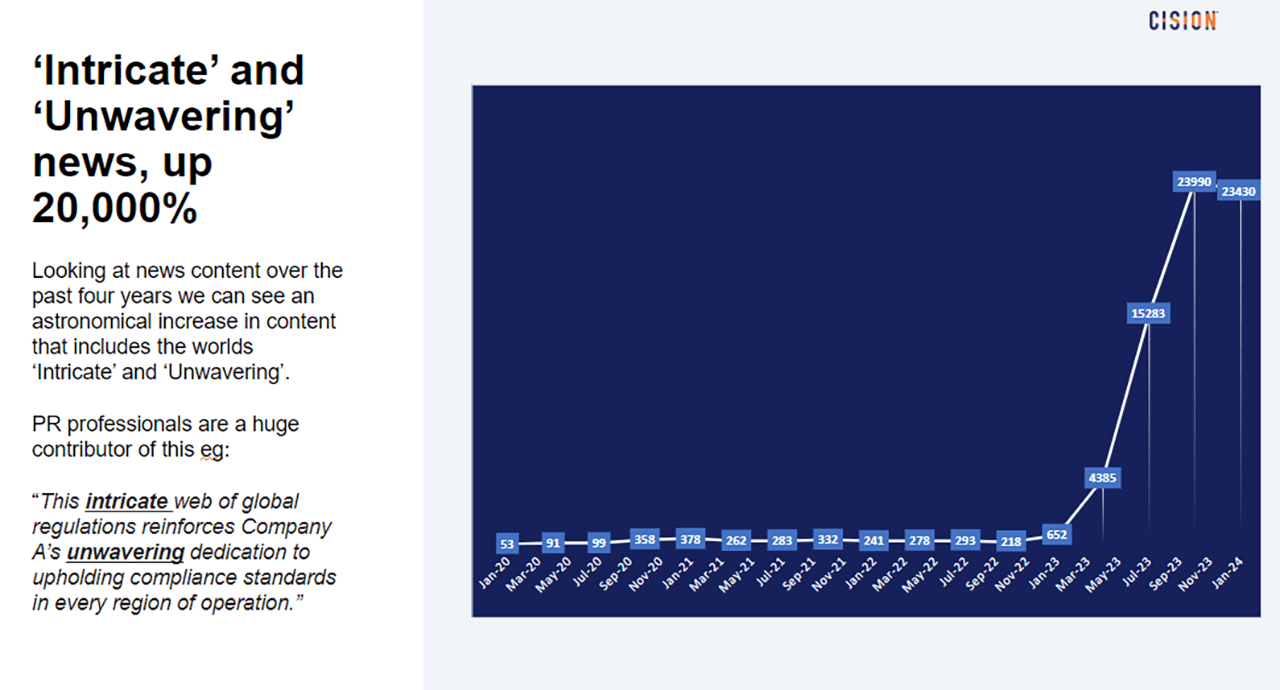

If these publishers (bloggers, newspapers, scientific research, how-to articles, etc.) no longer exist, or are less incentivized to create high-quality content due to cost savings, the consequences are dire. The pool of information that search engines rely on would become increasingly scarce, or diminish in quality and diversity. As publishers struggle to monetize their efforts, the incentive to invest in high-quality content creation wanes. This scarcity could lead to a homogenized internet landscape dominated by AI-generated content, which often lacks the depth, nuance, and originality that human creators provide. Ryan Broderick writes in Fast Company: “Why even bother making new websites if no one’s going to see them?”

Figure: Source Cision

As revenue becomes increasingly sparse, its understandable that (though these publishers will never admit to it) LLMs are very much generating content on their platforms. Either as a first draft or final draft, publishers first used the AIs to help produce for their long tail (SKU descriptions, sports coverage, etc). As we get more and more AIs publishing, the Dead Internet conspiracy becomes even more real. G/O Media faced social media backlash for using AI to produce articles in 2024, with readers describing the move as “pure corporate grossness” and criticizing the publication of “error-filled bot-authored content.” They ended up selling almost all their portfolio newspapers (including The Onion to my mentor Jeff Lawson, hi jeff <3) and laying off much of their staff. Similarly, when CNET published AI-generated articles without clear disclosure, leading to widespread criticism over factual errors and plagiarism. The controversy resulted in staff layoffs, unionization efforts, and a significant devaluation of the brand. In August 2024, Ziff Davis acquired CNET for 100 million USD, a stark drop from its previous valuation ($1.8B).

Quick Math

Ok lets recapulate and determine just how much $ is up in the air.

Lets deconstruct the global digital advertising market into the affected products. In 2023, Google’s share of digital advertising revenues worldwide was projected to amount to 39 percent. Facebook followed with a projected digital ad revenue share of 18 percent, while Amazon came in third with an expected seven percent. The player from Asia with the highest share is TikTok, with three percent, followed by Baidu, JD.com, as well as Tencent, all three with two percent. Lets break that down.

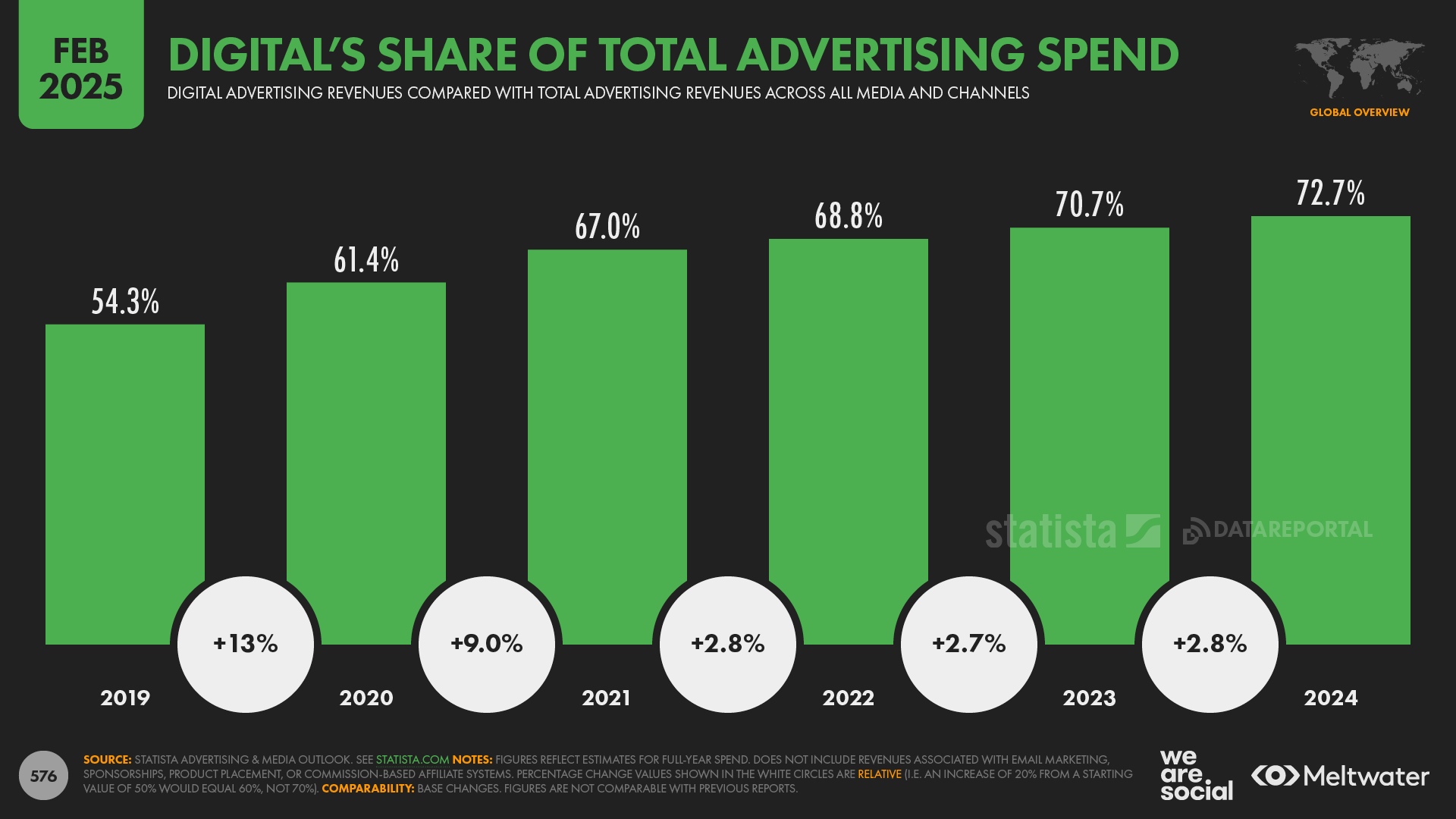

Global ad spend hit $1.1 trillion in 2024.

Digital formats account for roughly 72.7% of total ad spend, i.e. $790 billion.

Figure: Source Cision

We can split this into two major spend types: search (SERP) and display (banners, rich media, video).

search ads

Figure: Source Cision

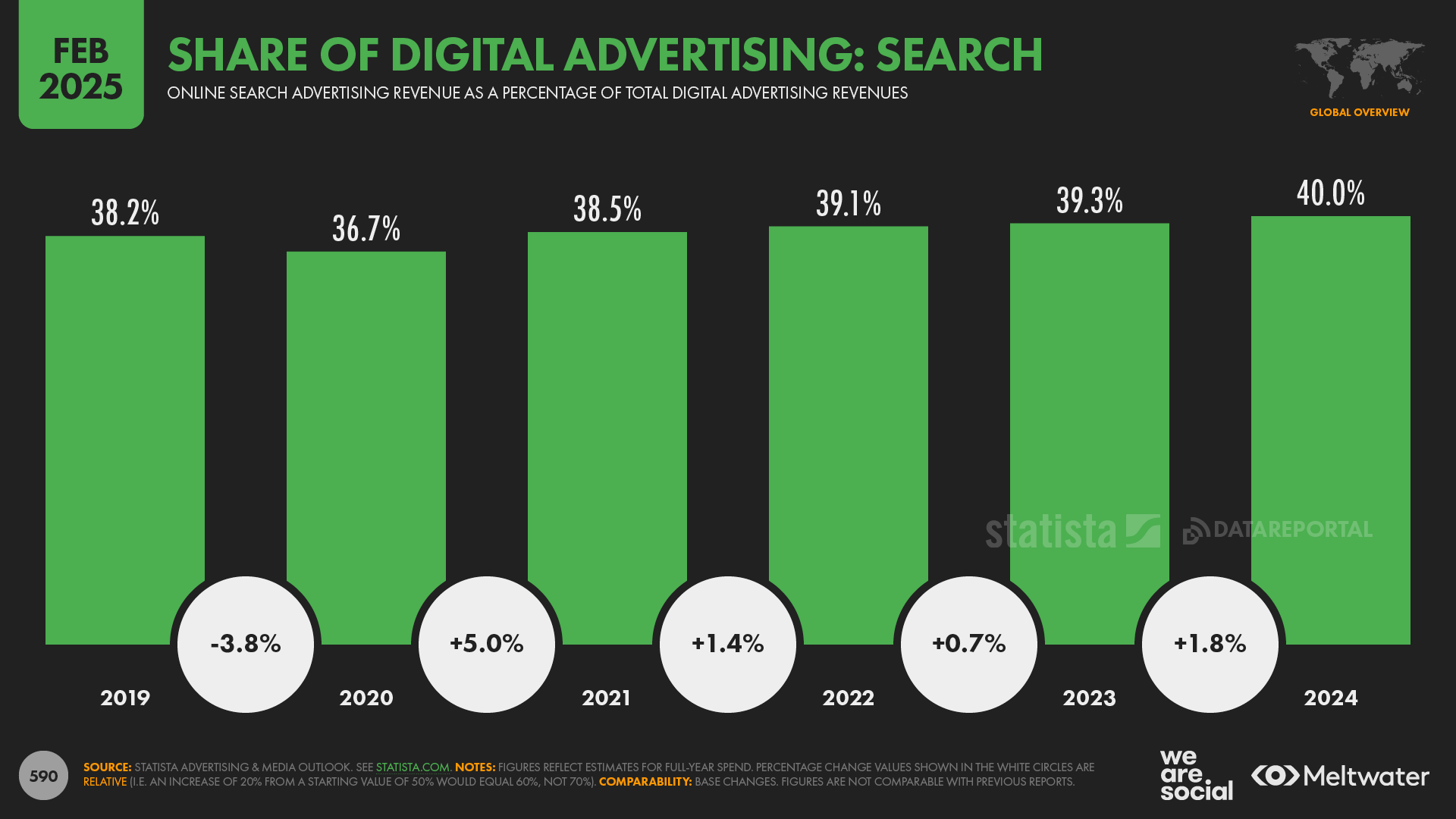

Obviously, all these numbers are estimates but statista claims 40% of digital spend goes to search, emarketer says 41.5%, and oberlo says 41.4% which means its somewhere in that ballpark. lets just go with the conservative numbers → $316 B

2025 search marketshare, has Google: 89.66% Bing: 3.88% Yandex: 2.53% Yahoo: 1.32% DuckDuckGo: 0.84% Baidu: 0.72% Others: 1.05%. But you can’t just distribute the add spend proportionally, since that would omit the other major search platform, retail.

According to eMarketer, 49% of Internet shoppers start their searches on Amazon, and only 22% on Google; Amazon’s share is far higher for Prime subscribers, which include over half of U.S. households.

Putting it altogether:

| Search Platform | Ad Spend (2024) | Reference |

|---|---|---|

| Google Search (SERP) | $198.1 B | Alphabet 2024 Annual Report |

| Amazon on-site Search | $56.22 B | Jungle Scout: Sponsored Products ≈ 78 % |

| Alibaba on-site Search | $25.2 B | Encodify: $42 B; 60%? is on-site search |

| Walmart Connect Search | $3.5 B | AdExchanger: $4.4 B global ad rev; 80%? on-site search |

| eBay Promoted Listings | $1.47 B | eBay Q4 “first-party ads” $368 M × 4 quarters |

| Target | $0.49 B | Marketing Dive: $649 M Roundel rev; 75%? is product-ad/search |

| Other search engines and retailers (Bing, Yandex, Baidu, etc) |

$43.4 B | Remainder |

| Totals | $316 B |

all of this is going to be seriously challenged by the AI Search renaissance.

display ads

Display ads (banners, rich media, video) represent about 56.4% of digital spend → $461.07 billion.

By 2025 programmatic channels will handle 90% of display ad budgets; assuming a similar rate for 2024, that was roughly $414.96 billion in programmatic display spend

Global affiliate marketing spend (performance-based links driving publisher commissions) will exceed $15.7 billion in 2024

Sponsored content (native, branded articles/videos) in the US alone tops $8.14 billion this year

In total, the combined spending on display ads, programmatic channels, affiliate marketing, and sponsored content is ~$438.8 billion in 2024.

Ad tech fees (exchanges, SSPs, DSPs) typically consume ~30% of programmatic budgets. If publishers capture the other ~70%, that implies 438.8B × 0.7 ≈ $307.16 billion in programmatic display‐ad revenue flowing to publishers. The flip of this is the 131.64B in revenue that the ad industry doesn’t get either.

to single out google’s AdSense for Content program, publishers keep about 68% percent of the revenue. Which, if Google’s programmatic‐platform market share is 28.6% → 111.5 B, publishers receive ~$75.8 B.

According to Gamob, Google’s search revenue sharing network, The Search Partner (AdSense for Search) represents roughly 10% of google’s total revenue. According to the actual 2024 anual report filing, it was closer to 8.67% ($30.36B). Publishers earn 51% of partner-network ad revenue → $15.18 B. Yandex, Yahoo, etc., offer limited or no comparable search-partner revenue-share programs, so we treat their downstream to external publishers as negligible for this estimate.

If we add google’s 198.08B from search, 30.36B from display and youtube/CTV’s 36.15B, it precisely equates to the 61659+64616+65854+72461=$264.59B in 2024 ad revenue we had in the figure back when we were discussing the slowing 8.47% YoY Growth in ad revenue, mitigated by increasing CPC costs. beautiful. whats gonna happen to it? what about these other companies?

Figure: Source: math + claude viz

where to next?

ok so the economic model of the internet is broken. #genz yay 🙄

the incentives of publishers are no longer to produce high quality content, unless they want to game the algorithm to rank higher in AI Overviews (Generative Engine Optimization) and/or sign a faustian contract to let the algorithms pilage their articles.

when we look for information on the internet, the AI Overviews are not truthful not useful when they give us suboptimal or entirely false answers in the pursuit of ad placements or serving a majority of users.

All that was back when we were using human interfaces - increasingly so, agents are interfacing with the internet on our behalf.

Plus, whats gonna happen to the $316B in search spend? What will Proctor & Gamble gamble on? What will happen to the publishers that are no longer rewarded for web traffic with (~100B in) revenue sharing, and more importantly, can no longer (up)sell their products via their website?

trends

one of the ways to figure out what to do next is to see where things are heading more generally. we should look at what is possible now that previously wasn’t possible due to the advent or convergence of multiple innovations that collectively lead to generational companies. The lineage lines are very clear if you know your history:

Alexander Bell’s advent of the telephone in 1876 came off the convergence of telegraphy (morse code) adoption, electrification progress and the increasingly cheap railroad/wood costs to build poles that could vary the intensity of electric currents to replicate sound waves. With this development of electric signal broadcasting infrastructure, and the utility of instant communicatiton in WW1, broadcasting voice to many users (not just 1-1) was quickly adopted leading to radio’s pervasiveness. 40 years later as cost of producing visual media fell (e.g. photographs instead of paintings), it became more feasible to transmit not just voice but also images over long distances, leading to the first television broadcasts. Early television systems used mechanical methods, such as spinning disks, to scan and display images. With Steven Sasson’s (1975) realization that images could be captured AND stored electronically (by using a increasingly cheap CCD image sensors) he packaged the nobel prize invention with cassete tapes into a toaster sized 8lb portable digital camera.

The Bell Telephone Company established a vast conglomerate and monopoly in telecommunication services until ‘Ma Bell’ was forced to break up in 1982 due to antitrust regulations. This monopoly was based on the pre-allocation of network bandwidth, which involved assigning radio frequencies to different applications. During the Cold War, to prevent the public broadcasting of sensitive data, DARPA initiated the development of ARPANET. ARPANET was built on the foundation of packet-switching, TCP/IP protocols, and IMP routers. This ‘alternative’ to traditional telecommunications was progressively adopted by the university researchers that created it and eventually led to the creation of the web as we know it today. As mentioned earlier, it was important that these data packets sent and received were legible, so Tim Berners-Lee’s developed aa global hypertext system for information sharing. That information, text, voice or the now digial images ‘permitted’ Napster to share music files over the internet from one ‘peer-to-peer’. It was a shortlived movement, from 1999-2001 but revealed the public’s hunger for on-demand, personalized, frictionless access to media, decoupled (decentralized) from traditional broadcast and retail gatekeepers.

But what if, instead of downloading the (music/text/etc) data packets to my floppy disks, I could just host media on the public web and have people stream directly? Great question, YouTube founders. In 2005, as internet bandwidth became capable of file transfers at megabits per second, and Macromedia’s (later, Adobe) 1996 invention of Flash (RIP 1996-2020) enabled interactive websites, simple upload-and-share interfaces democratized video (text/music/etc) publishing while its streaming capabilities eliminated the need for complete downloads before viewing. In 2007, a certain turtlenecked individual merged all of the progress that made PCs more affordable/compute efficient, a digital camera, telephony compliance and internet browsing into (you guessed it) the iPhone. All founders have to mention it at some point, forgive me, but hopefully you can see why its such a landmark moment. Take a moment to bask:

Figure: Source: Evan Fenster on X the everything app

The iPhone revolution, via its app store, permitted social graphs, image sharing and instant news/information sharing that still struggles to satiate the public thirst. Driven by the now vast data published, cloud-distributed computing resources, and rehashed algorithmic research from the 70s, machines could learn patterns (in images, search intent, or entertainment). Its gotten to the point that it can even generate its own entertaining media, or answers to search queries as we very well know by now.

toys

The reason big new things sneak by incumbents is that the next big thing always starts out being dismissed as a “toy.” This is one of the main insights of Clay Christensen’s “disruptive technology” theory. This theory starts with the observation that technologies tend to get better at a faster rate than users’ needs increase. From this simple insight follows all kinds of interesting conclusions about how markets and products change over time.

Disruptive technologies are dismissed as toys because when they are first launched they “undershoot” user needs. The first telephone could only carry voices a mile or two. The leading telco of the time, Western Union, passed on acquiring the phone because they didn’t see how it could possibly be useful to businesses and railroads – their primary customers. What they failed to anticipate was how rapidly telephone technology and infrastructure would improve (technology adoption is usually non-linear due to so-called complementary network effects).

The same was true of how mainframe companies viewed the PC (microcomputer). Initially, PCs were seen as toys for hobbyists, incapable of the kinds of serious business applications that IBM handled. Yet, as software and hardware rapidly improved along the exponential curve of fabs doubling the number of transistors on a microchip approximately every two years, PCs became indispensable tools in both personal and professional settings.

Kodak made a lot of money with very good margins providing silver halide film; digital cameras, on the other hand, were digital, which means they didn’t need film at all. Kodak’s management was thus very incentivized to convince themselves that digital cameras would only ever be for amateurs. Kodak filed for bankrupcy in 2012.

YouTube’s early days featured grainy, amateur videos that serious media companies considered amateurish and irrelevant. “Broadcast yourself” seemed like a frivolous concept when the first videos were cats playing piano and awkward vlogs.

The first iPhone was ridiculed by BlackBerry executives for its poor battery life, virtual keyboard, and limited enterprise features. “It’s a toy for consumers,” panned by the likes of Microsoft’s Steve Ballmer — who laughed off its lack of a physical keyboard.

Early apps were basic utilities and games like “iBeer” (a virtual glass of beer) or keeping the flashlight on. Friendster, MySpace, and Facebook were considered trivial diversions for teenagers — mere digital yearbooks with Farmville and the ability to “poke” each other. Established media companies and advertisers dismissed them as fads, failing to see how these networks would become primary channels for news distribution, customer engagement, and political discourse. Steve Jobs saw right through this, watch this launch of Garageband:

Figure: Source: Evan Fenster on X the everything app

[12:24] I’m blown away with this stuff. Playing your own instruments, or using the smart instruments, anyone can make music now, in something that’s this thick and weighs 1.3 pounds. It’s unbelievable. GarageBand for iPad. Great set of features — again, this is no toy. This is something you can really use for real work. This is something that, I cannot tell you, how many hours teenagers are going to spend making music with this, and teaching themselves about music with this.

A couple years later, facebook left the world wide web to go mobile native. They were pegged as a way to play toy apps and video games. From TechCrunch in 2012:

Facebook is making a big bet on the app economy, and wants to be the top source of discovery outside of the app stores. The mobile app install ads let developers buy tiles that promote their apps in the Facebook mobile news feed (e.g. Farmville, Plants vs Zombies). When tapped, these instantly open the Apple App Store or Google Play market where users can download apps.

Much of the criticism of app install ads rests on obsolete assumptions that view apps as fun baubles instead of the dominant interaction layer between companies and consumers. If you start with the premise that apps are more important than web pages or any other form of interaction when it comes to connecting with consumers, being the dominant channel for app installs seems downright safe.

https://stratechery.com/2015/daily-update-bill-gurley-wrong-facebook-youtubes-competition/

Almost all early efforts of AI were to play recreational games like chess, Go, and poker. OpenAI started by training models to beat DoTA champions. These EXACT same algorithms power website ranking elos, protein folding research, and ChatGPT’s reasoning models. LLMs started with recipes and toy use cases but are maturing into enterprise use cases (starting, of course, with “fresh grad” tasks). the landmark AI Agent paper was about playing minecraft, and you can go watch Claude Play Pokemon right now.

Disruptive innovation is, at least in the beginning, not as good as what already exists; that’s why it is easily dismissed by managers who can avoid thinking about the business model challenges by (correctly!) telling themselves that their current product is better. The problem, of course, is that the disruptive product gets better, even as the incumbent’s product becomes ever more bloated and hard to use. That, though, ought only increase the concern for Google’s management that generative AI may, in the specific context of search, represent a disruptive innovation instead of a sustaining one.

AI

It’s become increasingly clear that AI is not a toy, and will become a defining pillar for the next generation of coalescing trends. We’ll explore many more in the future, but lets focus on AI first and foremost.

I’m not going to go into the history of AI because it’s pretty well known at this point and tbh not super helpful for the unfolding of the agentic web. What I will do, is define Artifical as ‘nonhuman’, and borrow the definition of Intelligence from Jeff Hawkins’ theory of the brain in A Thousand Brains: A New Theory of Intelligence. Hawkins writes: